We need to look at additional metrics of pension well-being as pension funds struggle with the triple-whammy of rising liabilities, falling asset values, and diminished ability to close the underfunding gap with accelerated contributions.

In particular, fund administrators should look beyond the subjective actuarial return assumption to both the risk-free rate of return and the required rate of return. The former highlights the reliance on assumed investment gains to meet fund liabilities, and the latter, if an impossibly high return, is a wake-up call that tough decisions are needed now on how to fund future liabilities.

We should know all of these figures on a per capita or per employee basis. Taking the numbers to a human scale helps us to better understand the magnitude of the challenges we face.

The underfunding gap has been growing for a quarter-century, but has widened dramatically in the wake of the Covid-19 market crash. The economic reality is that unfunded liabilities have already soared, but pension funding reports have not yet caught up with that reality.

Between mid-February and late March 2020, we saw a “take no prisoners” market crash. Anything with a whiff of perceived risk crashed, in direct proportion to its perceived risk. The only assets that soared—because of tumbling interest rates—were long Treasury bonds, and with them, the net present value of pension obligations. The catalyst was, of course, the growing recognition that an economic lockdown, intended to mitigate the spread of the COVID-19 virus, was going to have an extreme and lasting impact on the global economy.

Today is still self-evidently early days in the economic rout created by the COVID lockdown, and perhaps middle days in the health consequences of the virus. This ordeal, the policy choices we have made, and the health and economic impacts of those choices, will likely be studied for generations to come. After all, in the history of our country, we have never deliberately imposed an economic lockdown, not because of a pandemic such as the AIDS epidemic (with 32 million deaths globally, and counting), the Spanish flu of 1918–19 (50 million or more deaths), the Asian flu and polio epidemics of the 1950s (well over 1 million deaths each), nor because of world wars. Many of our readers will know my view, that it was never a choice between saving lives and saving the economy. We could have chosen to do both, as the East Asian democracies have proven.1 But, that’s not the point of this short article.

This article will focus on the impact of the COVID crash and economic dislocations on pension funding and on the resources available to present and future retirees. At a time when the resources available for pension contributions (tax revenues for public funds and company profits for corporate pensions) are in free-fall, pension administrators are faced with a triple-whammy of rising liabilities, falling asset values, and diminished ability—likely for some years into the future—to close the gap with accelerated contributions.

In writing this article, I’m not seeking to annoy the many pension sponsors who we count among our clients and friends. I know pension funding ratios are a controversial topic, even a lightning rod. Rather, I’m asking our industry to study additional metrics of pension well-being that can give us a richer understanding of the pension problem, sharply exacerbated in a single quarter by a drop in asset values and a sharp rise in the net present value of future pension obligations.

Consequences of the COVID-Inspired Economic Lockdown

Many consequences are associated with the economic lockdown and the capital market shocks triggered by the lockdown. A short list of the effects already being explored in serious academic circles and by the media might include:

- Of the 30 million businesses in the United States, most of which have one to five employees, how many will not survive the lockdown and its aftermath? Time will tell, but it is likely to be many millions.

- How many of the 40 million who lost their jobs in the first 10 weeks of the lockdown—25% of the labor force—no longer have a job to return to?

- A healthy entrepreneurial economy will replace these businesses if they are still needed in a post-COVID world and will create new jobs for anyone willing to work—but it will take time.

- If everyone is bailed out, no one is bailed out. Who are the net beneficiaries, and who are the net losers, in the multi-trillion-dollar stimulus packages that seemingly seek to bail out everyone who is suffering? Who pays for it? When and how?

- What’s the impact on public and corporate debt, domestically and internationally, and how will we collectively service this debt? Debt can be serviced, renegotiated, or canceled (through default or through inflation). These choices affect borrowers and lenders alike; either side can trigger far-reaching domino effects—externalities—if the debt cannot be serviced. (This is the reason the EU did not permit Greece to default on its debts or to leave the euro.)

- When do we return to our travel plans, our hotels and restaurants, our shopping malls, sports arenas and concerts? If COVID has lasting effects on our willingness to dine out, travel for business or pleasure, what will happen to these industries and their legions of employees?

- Will we need all of our existing office space now that we find many businesses can be fully productive with their employees’ working from home? As Nobel Laureate Vernon Smith (2020) points out in a recent Wall Street Journal op-ed, many of these buildings can be repurposed, but that will take time.

Our attention is currently focused, of course, on the immediate impact of the COVID crisis; however, the long-term effects also merit thoughtful attention. The health of the pension industry and the vast and growing scale of unfunded obligations have been much in the news in recent years. The COVID crash arguably did more damage to pension funding health than any of the market’s moves since the crash of 2008, wiping out the intervening decade of (inadequate) funding progress.

The Impact on Pension Funds and Pensioners

The media and academia are enjoying a lively debate about whether near-zero interest rates are good, bad, or indifferent for the economy at large. There is no debate, however, about the dire impact low rates have on our savings and on those who rely on a fixed income, notably pensioners.

In 2004, Jim Garland and I independently published work on a concept that I called “sustainable spending” (Arnott, 2004) and he called “portfolio fecundity” (Garland, 2005). This concept relates to the income stream a portfolio can sustain over its intended span. For a retiree, this can be framed simply as, how much money can I spend each year, over perhaps 20 or more years, presumably adjusted for inflation, without running out of money?

We cannot know our sustainable spending level without reasonable estimates of four things:

- the size of our portfolio,

- our intended future spending plans, including their duration,

- the real returns we can reasonably expect to earn over that span, and

- the likely trajectory of inflation, fees, and taxes in eroding our future spending power.

To state the obvious, more money in our retirement portfolios will proportionally allow for more spending, as will higher real returns on our assets. When bonds offer negative real yields, stocks are at lofty valuation multiples, and vast deficits drive tax rates higher, our forward-looking returns are lousy, as is the sustainable spending that each dollar of assets can sustain.

Broadening the question for a pension fund, with thousands, or even millions, of prospective beneficiaries, the same question applies, but with perhaps a 60-year (or longer) horizon to cover costs for the youngest of our future retirees. That said, the first 20 years are where most of the obligations typically reside.

The “Take No Prisoners” Market Crash

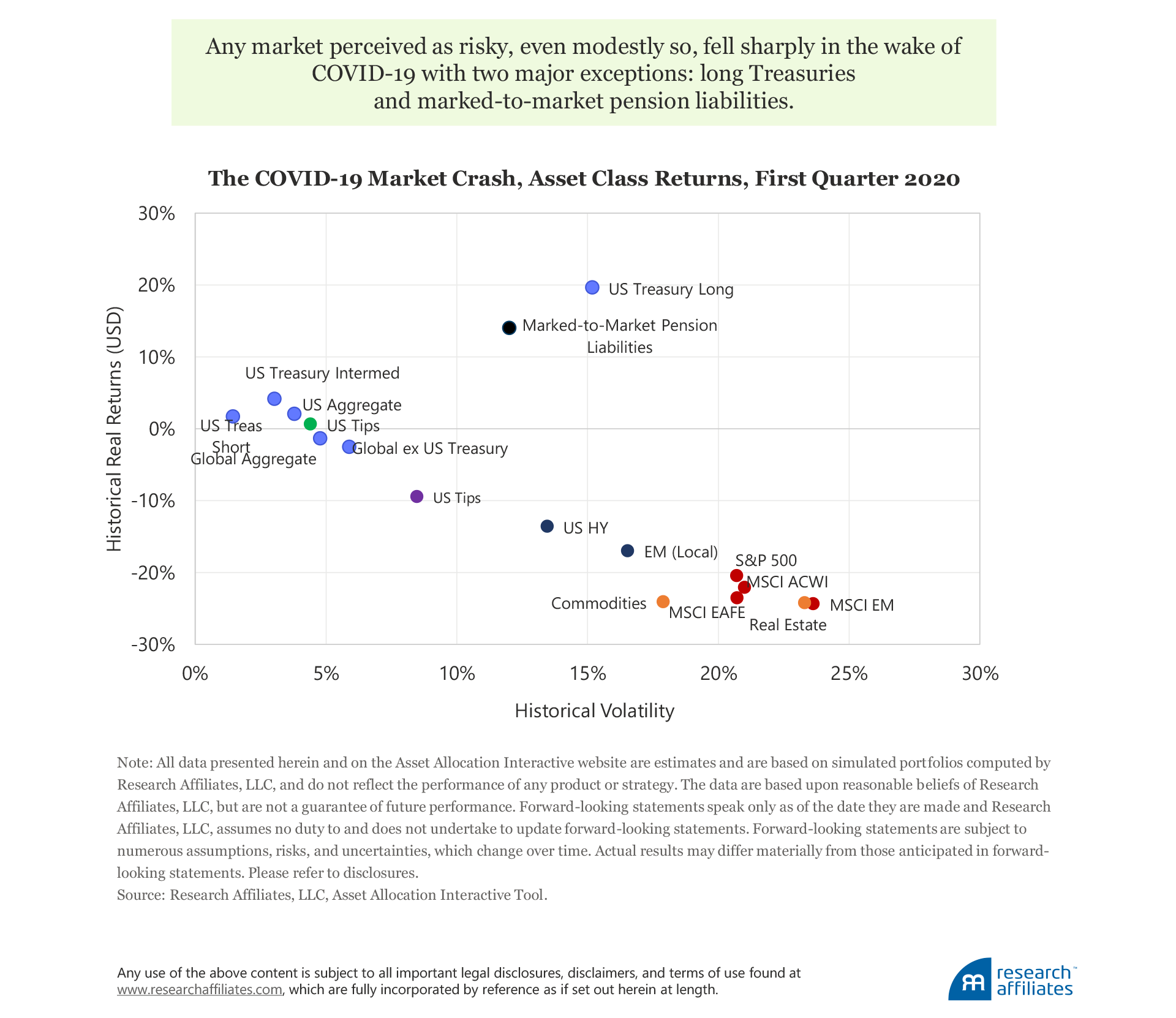

In the first quarter of 2020, any market perceived as risky, even modestly so, fell sharply. Although these markets recovered some considerable lost ground from the closing days of March through May, the February–March crash generally took them down in direct proportion to their historical risk. US small-cap stocks, measured by the Russell 2000 Index, fell by 30%, matching the standard deviation of the past year for that market. The NAREIT Index fell 24% against 24% risk; the S&P 500 Index fell 19% against 19% risk; and so forth. The only major outliers were long Treasuries, up 20% against 15% risk, and marked-to-market pension liabilities up 14% against 12% risk. Wow.

Is this unprecedented behavior? No. It’s actually typical of market crashes. We saw much the same in October 1987 and September–November 2008. In both cases, essentially all risky assets cratered in rough proportion to their perceived risks, while Treasury bonds soared.

Why are market crashes so indiscriminate? Crash conditions lead to a very fast sorting out by investors—even very large institutional investors—of who wants less-risky assets and who is willing to own more-risky assets at a newly lower price. Because there are far more of the former than the latter, the price falls to a point where the willing buyers match the newly risk-averse sellers. There’s little time to carefully evaluate which markets are cheaper than warranted in the new economic conditions and which markets are not yet cheap even after the crash.

The aftermath in each case was a sorting-out process, with investors seeking to gauge which markets had been hit beyond reason and which markets were still not cheap, even after the crash. We believe we will see that sort of behavior in the months ahead.2

The Abandonment of the Pensioner

I’ve long been on record as suggesting society cannot easily afford for my generation, the baby boomers, to retire at the same age and on the same retirement income (relative to our earned income) as our parents (Arnott and Casscells, 2003, Arnott and Chaves, 2013, and Arnott, 2015). There are too many of us, and unlike our parents, most of us had relatively few kids. What cannot happen will not happen. Zero interest rates were already breaking the deal. Who knew that COVID might be the catalyst that finishes the job?

I’ve long thought our accounting for pension promises was incomplete (Arnott, 2004). In corporate accounting, we use a pension return assumption to calculate pension expense according to GAAP, and we use an actuarial discount rate based on AA bond yields to gauge funding ratios and prospective contribution requirements. In the public fund arena, we use only an actuarial discount rate, which is often referred to as the actuarial rate of return (ARR), because it is generally viewed as the expected return on public pension fund assets. If public pension assets earn a future return that falls short relative to the actuarial discount rate, which I’ll refer to in this article as the return assumption, the tacit presumption is that higher pension contributions can close the gap later.

As a result, institutional pressures encourage a high return assumption. After all, the higher the assumed return, the better the funding ratio will seem and the lower the contribution that is needed. An actuary or accountant who insists on a low return assumption will not get many job offers. Of course, choosing a particular return assumption is no guarantee it will actually be earned.

Those tasked with shepherding our public and corporate pension funds strive mightily to achieve these target returns and are often judged harshly if results fall short, even when the return target was implausible to begin with. They are understandably distressed that mainstream investment portfolios might not achieve this return, and even more distressed at the notion they have to deliver results that are higher even than the return assumption.

Metrics for Pension Health

We might sensibly view pension assets and liabilities as having a number of relevant metrics, which can be thought of as portfolio return metrics and can be expressed in terms of dollars per employee or, for public pensions, dollars per citizen.

Let’s first look at these issues through the prism of the pension return assumption. My goal is not to be controversial, but to point out that we can have a much richer dialogue about pension policy, and make sounder choices, if we know these three return numbers: the risk-free return, the return assumption chosen by the funds’ accountants and actuaries, and the required return. The pension community generally chooses to ignore the first and last metric, both of which are objective measures, and to focus on the return assumption:

Risk-Free Rate.3 This is the risk-free rate that a fund can—with near certainty—earn on its assets between the present and the future dates it expects to pay its pension obligations. The risk-free rate is not the yield a Treasury bill offers. The risk-free rate is based on the yield of a Treasury bond or TIPS (Treasury Inflation-Protected Security) with a duration similar to the duration of the pension obligations.4 For simplicity, I use the Treasury bond yield, not the TIPS yield, but the rate should ideally be a blend of the two to reflect the extent to which future distributions will likely be impacted by inflation.

Return Assumption. This rate is a subjective forecast by pension accountants and actuaries of likely future investment returns. Corporate pensions call this the pension return assumption (supplemented by a bond-market-based discount rate for pension funding calculations), and public funds call it the actuarial discount rate or actuarial rate of return.

Required Return. This is the rate of return pension assets must earn to fully service the pension fund’s liabilities, or obligations, without raising the level of contributions to the pension fund. As much as pension administrators would like pension obligations to be paid solely by investing in the capital markets, it is naïve to believe pension obligations can be met without funding them!

The typical reaction to the notion of discounting future liabilities using a risk-free rate is: “That’s stupid… of course the pension fund will earn more than this rate.” This argument is sensible and powerful, but it still makes sense to know the risk-free rate. The gap between the risk-free rate and the pension return assumption is the amount fund managers implicitly assume their investment prowess will add over, and above, the risk-free rate.

Any return earned above the risk-free rate is, by definition, either a risk premium or skill-based alpha. The long-term excess return of stocks, relative to Treasuries, is a good example of a risk premium; we call it a risk premium because stocks are riskier. Specifically, stocks have downside risk, even at times when liabilities are soaring.

In 2002, Peter Bernstein and I documented in the Graham and Dodd award–winning article “What Risk Premium Is ‘Normal’?” that the normal equity risk premium is around 2.4%, not the 5% that many then assumed. Indeed, 10- and 20-year Treasury bonds have beat US stocks over the past 20 years (by 70 and 200 basis points a year, respectively)—yet investors still expect 5% more return from their stocks than from their bonds!

Meanwhile, the quest for alpha—beating the chosen market benchmark on a risk-adjusted basis—is inherently a zero-sum game (minus fees and trading costs!). If all fund managers assume they will earn a positive alpha, at least half will be disappointed. This does not mean the quest for alpha is a waste of time. The sensible assumption for alpha is zero, however, until after the alpha is earned!

The drop in both the market value of risk assets and the risk-free yield during the COVID-induced market crash hurts both the asset and liability sides of the pension funding equation. The 20-year Treasury bond yield-to-maturity of 1.15% on March 31, 2020, was the lowest end-of-quarter yield in history. A pension sponsor who chooses to invest in these bonds would have hardly any uncertainty about how much can be distributed in future pension benefits, and hence, my labeling this the risk-free rate. Sadly, the pension assets would not cover much of the contractual pension obligations—but the fund manager would know the shortfall with some reasonable precision!

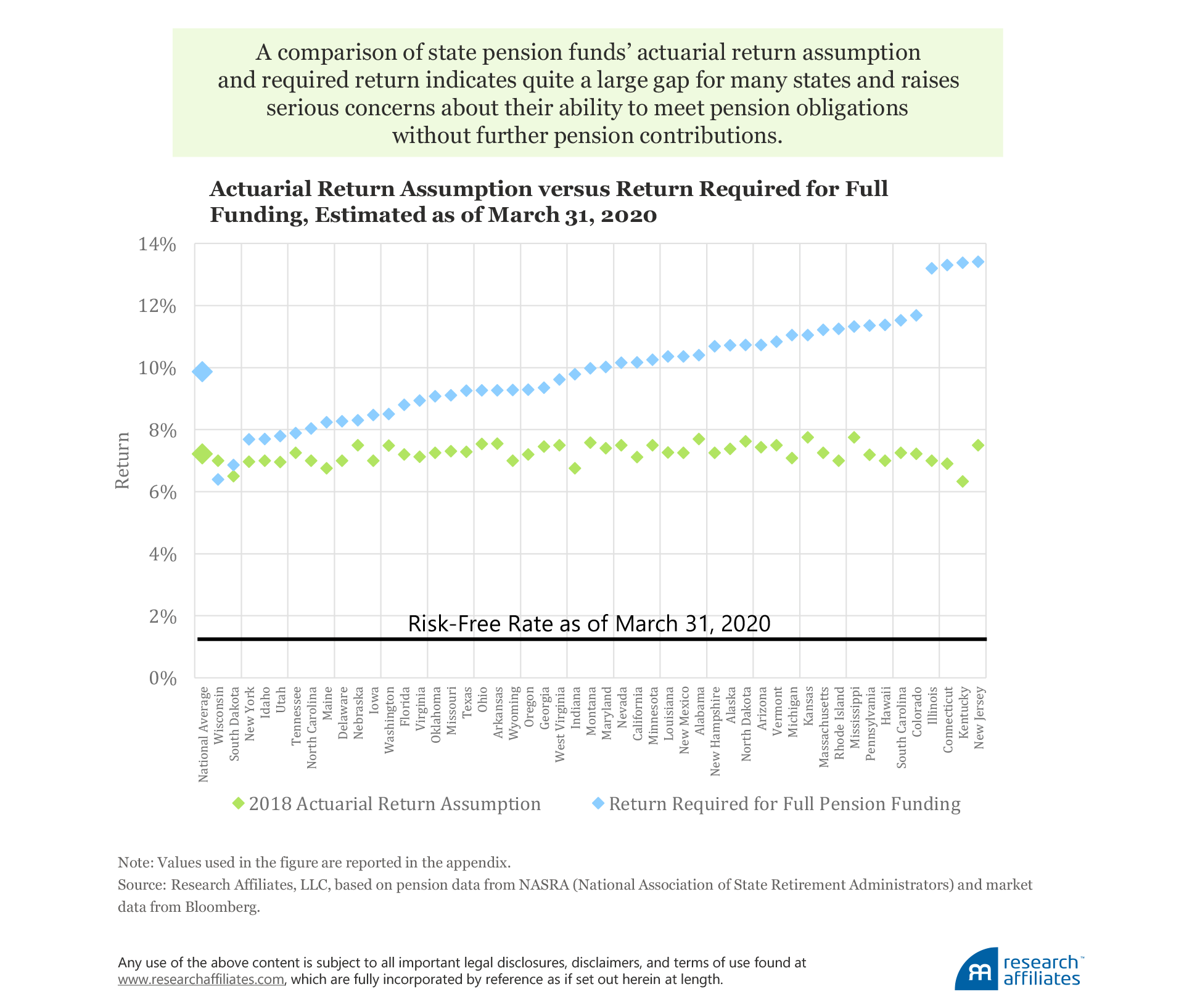

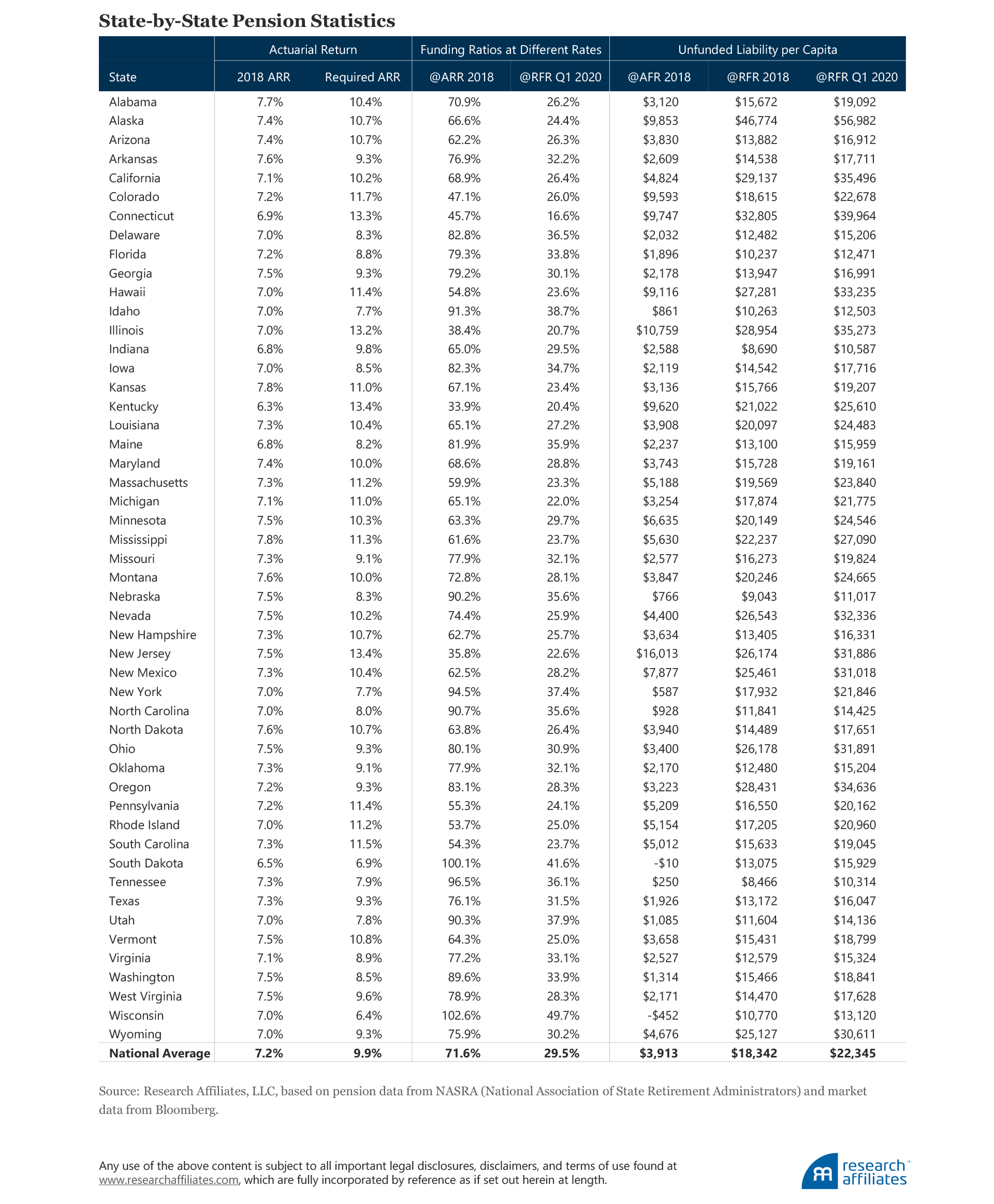

A comparison of the actuarial discount rates for each of the 50 states ranges from a low of 6.33% for Kentucky to a high of 7.75% for Kansas and Mississippi. The national average is 7.21%.6 In almost every state, these assumptions are well below the levels of 10 years ago. Corporate pension return assumptions are a bit lower on average, but fall in the much wider range of 4% to 9% (Wadia, Perry, and Clark, 2020), with an average of 6.5%.

If the current risk-free rate is 1.15%, a return assumption above 4% is aggressive. I am not going to second guess the states’ discount rate choices, other than to observe they are generally high relative to a world of near-zero bond yields and lofty Shiller PE ratios. On average, pension administrators are assuming the funds they manage will earn about a 6% excess return above the risk-free Treasury bond yield—a consequence of either a risk premium for bearing short-term downside risk or the zero-sum-game of skill-based alpha from beating the funds’ chosen market benchmarks.

We can contrast the actuarial return with the required return. If pension administrators can earn the required rate of return on pension assets, current fund assets will suffice to cover all projected pension obligations, with no increase in pension contributions above the current level recommended by the accountants and actuaries. The required returns across the pension funds of the 50 states also fall in a wide range, from 6.4% for Wisconsin (below the state’s discount rate of 7%, reflecting an actuarial funding ratio above 100% for the state) to a high of 13.4% for Kentucky and New Jersey.

Both public and corporate pension sponsors have been steadily reducing their return assumptions for nearly 20 years. They should be applauded for doing so. That said, if the return assumptions are still too high—and especially if the required return is considerably higher still—we may soon face the problem of the Red Queen in Lewis Carroll’s Through the Looking Glass: “Here, you see, it takes all the running you can do, to keep in the same place. If you want to get somewhere else, you must run at least twice as fast as that!”

Funding Ratios and the Abandonment of the Pensioner

The 2019 bond bull market lowered the 20-year Treasury bond yield from 2.87% to 2.25%, and the COVID-induced crash took the rate all the way down to 1.15% (after an intra-month low of 0.87% on March 9). If asset prices are lower and the risk-free discount rate for the liabilities is lower, we have a problem. I describe this problem as the abandonment of the pensioner.7

If we imagine a prorated share of the pension as one employee’s retirement savings, the problem is clear. The sustainable spending has tumbled, leaving the employee with the following choice: save more aggressively, retire later, retire on less income, or risk outliving the money—or a blend of the four. For funds with a low funding ratio or a high required return, pension administrators face the same four possibilities: contributions can be increased, now or eventually; age of eligibility for retirement can be raised, now or eventually; benefits can be cut, now or eventually; or the fund can risk running out of funds. If this happens, who is going to backstop the pensions, and are they similarly protected?

Each of these “fixes”—higher contributions or lower benefits—is far easier said than done. Each is controversial, pitting those who receive the benefits against those who fund the benefits. The most attractive option, earning the required return, is not on the list, because it’s implausible, although outsized returns are certainly possible with a sufficiently maverick portfolio. Aspiring to high returns provides no assurance we’ll earn them, which is perhaps the biggest problem with the return assumption: too many people believe that it’s reasonable to assume we can earn that target return merely because an accountant or actuary sets it as the return assumption.

These rates of return matter because they drive both the funding ratio and the estimated future contributions required to meet pension obligations. A higher pension return assumption (or actuarial discount rate) leads to a better-funded ratio, lower unfunded liabilities, and less future contributions. Again, setting a high return assumption doesn’t guarantee the return will be earned.

Using the return assumptions I defined in the previous section, we can measure the funding ratio (the ratio of assets to future pension obligations) in three different ways:

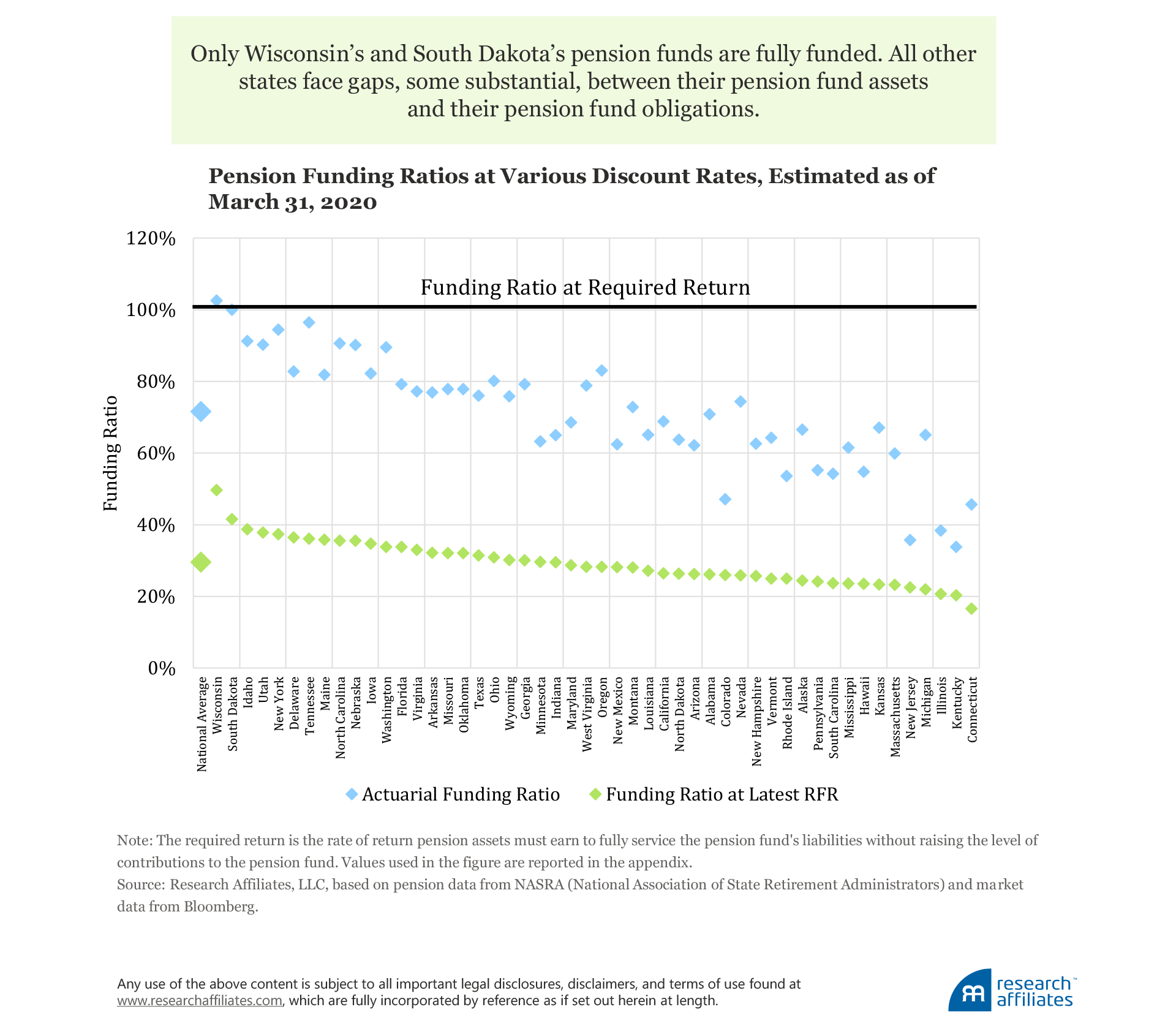

Official Funding Ratio: This funding ratio is based on the pension return assumption (or discount rate) recommended by the actuaries. These rates lead to a wide range of outcomes. For example, Wisconsin is 102.6% funded based on the official (or actuarial) funding ratio, but Kentucky is only 33.9% funded. The national average is 71.6%.

Risk-Free Funding Ratio: The worst plausible funding ratio for a pension fund is to earn the risk-free return. This can happen if the fund is managed in a hyper-conservative fashion as an immunized Treasury bond portfolio or if it fails to earn a risk premium or an alpha. The situation can get worse if the asset management delivers a combination of risk premium and alpha that is negative. The risk-free funding ratio ranges from 49.7% for Wisconsin to 16.6% for Connecticut. The average across the 50 states is 29.5%.

Required Return Funding Ratio: The required return is, by its very definition, the return at which the pension is fully funded.

Current practice narrows our attention to the first of these, the official funding ratio, which is the only return measure not objectively determined. In addition, pension administrators and boards should make a point of knowing the other two—the risk-free funding ratio and the official funding ratio—in order to have a more complete picture of pension health.

Consider Wisconsin. The state’s actuarial discount rate of 7% is equivalent to assuming that the state’s pension fund will earn 7% on its assets. If it does, the fund will be slightly overfunded at 102.6%. Splendid! But if pension assets fail to earn any premium over the current risk-free rate of 1.15%, then Wisconsin’s pensions are only 49.7% funded.

How can we intuitively understand the difference? Wisconsin’s obligations are halfway funded by current assets if invested in a risk-free immunized bond portfolio. We know (presume?) this is an unduly pessimistic outcome. The actuary is predicting that, as long as contributions continue at the recommended levels, the capital markets will fund the rest by providing a 7% annualized return, with a little room to spare.

For all other states, apart from South Dakota, the actuarial return assumption would need to be higher—often much higher—in order for the fund to be fully funded. This gap is the amount that must be closed by either contributing more to the pension fund, reducing distributions from the pension fund, or—implausibly, in my view—earning a long-term return even higher than the actuarial return assumption.

The national average of existing assets will cover a scant 29.5% of pension obligations if the assets are invested in a risk-free portfolio of Treasuries and TIPS. With an average return assumption of 7.21%, public pensions are 71.6% funded, on average. In effect, the nation’s actuaries and accountants are collectively projecting that excess returns from either risk premia or alpha will make up the difference, 42.1% of pension obligations, on average.

If the pension fund does not earn the 7.21% average target return, the actuaries and accountants are not on the hook for guessing wrong; that burden falls on the state’s taxpayers and/or prospective retirees. Even if the fund manages to earn the relatively lofty target return, pension beneficiaries and future taxpayers remain on the hook to close the last 28.4% of the total through reducing pension distributions or increasing contributions.

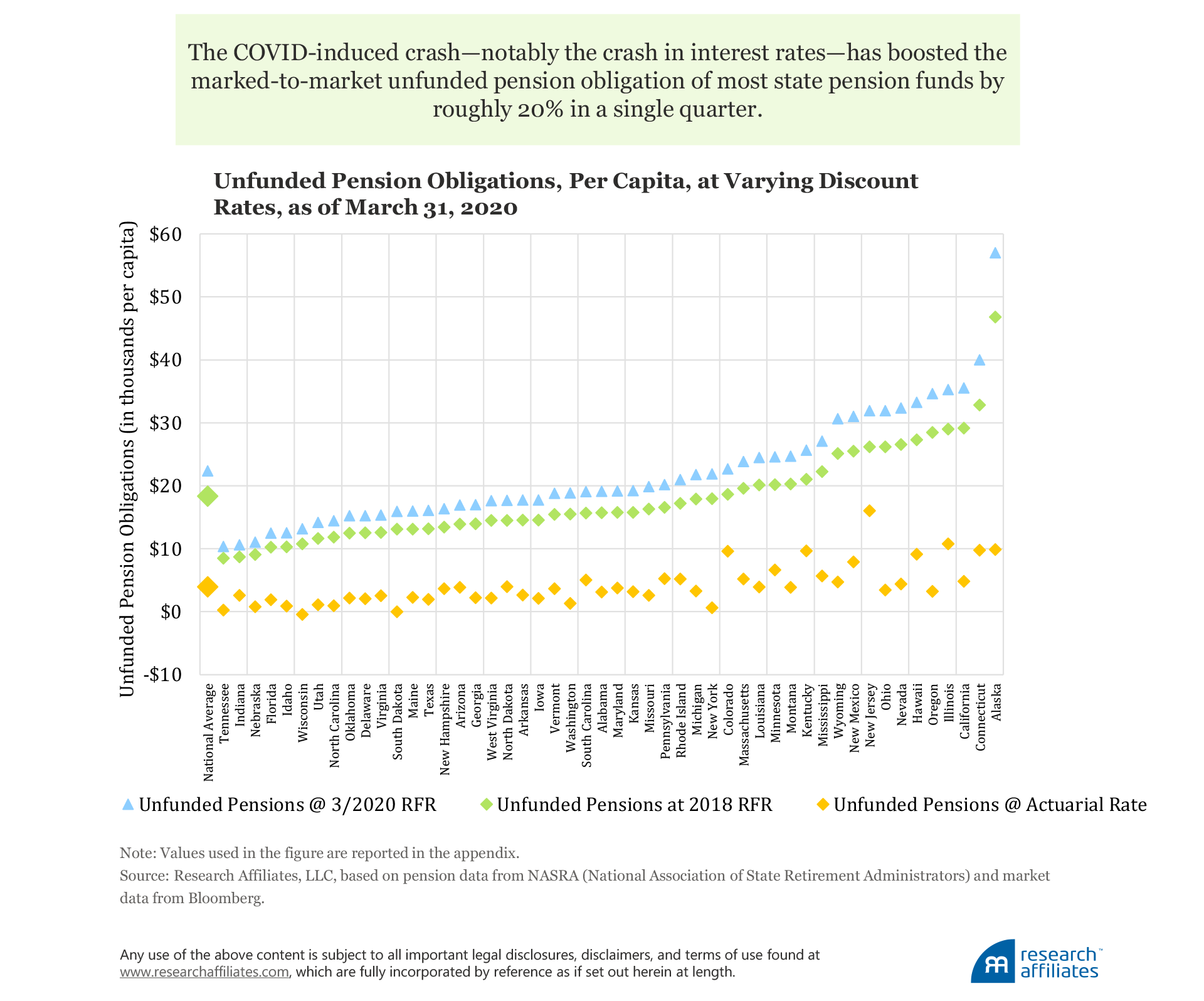

These rates of return and percentage funded ratios have real-world consequences that can be measured in dollar terms. It can be hard to wrap our heads around billions and trillions of dollars, so let’s look at the per capita dollar effects of the three funding ratios for state pension funds. Specifically, how large is the unfunded pension obligation expressed in dollars per resident of the state?

The official unfunded pension obligation, using the actuarial discount rate, ranges from $16,013 per state resident for New Jersey to –$452 (a surplus) for Wisconsin. The national average is $3,913 per state resident. This means that Wisconsin could send a check for $452 to every man, woman, and child in the state and still be fully funded. This assumes the pension fund earns its actuarial 7% discount rate, and contributions continue according to current formulas. New Jersey, however, would have to tap every man, woman, and child in the state $16,013 in order to instantly become fully funded at the state’s 7.5% actuarial rate.

The situation is not nearly as bad as it seems, however, because the pension liabilities extend decades into the future. For example, New Jersey could reduce other spending by $1,000 per state resident every year for a couple of decades into the future, divert these funds to the pension with a similar overall budget result, and not have to raise taxes—but that means fewer services for the state’s denizens.8 Even moderately serious underfunding can be a manageable problem if addressed early and the costs can be spread long enough into the future.

The magnitude of underfunding rises once we use a risk-free rate. At the year-end 2018 risk-free rate of 2.87%, underfunding ranges from $8,466 per state resident for Tennessee to $32,805 for California and to $46,774 for Alaska, averaging $18,432 per resident nationwide.9 Let me stress that these numbers are, by design, worst-case figures, because any pension can de-risk to the point of holding only Treasury bonds and TIPS. If pensions earn less than their actuarial return assumption and more than the risk-free rate, the cost of making up the shortfall lies in that midrange, too. The shortfall can be closed by using any mix of diminished benefits, such as increased employee contributions, increased employer contributions, or simply earning higher pension fund returns than appears plausible at current valuation levels.

We can also look at how the unfunded liability has changed solely because risk-free bond yields have steadily fallen since 2018; it bears mention that 60% of the drop has occurred in the first quarter of 2020. Using the 1.15% risk-free rate as of March 31, 2020, the per capita unfunded liability for Tennessee rises from $8,466 (calculated using the year-end 2018 risk-free rate) to $10,314, and for California and Alaska rises from $32,805 to $39,964 and from $46,774 to $56,982, respectively. The per capita average rises from $18,342 to $22,345.10

On a marked-to-market basis, the COVID-induced crash in bond yields has cost the average US family of four $16,000 in additional future pension obligations, taking the total in unfunded obligations per family to a national average of nearly $90,000. In Tennessee, the additional pension obligation attributable to the COVID crash works out to $7,400 per family and in Alaska the pension obligation jumped by $49,000 per family over a few short weeks! The gap doesn’t need to be closed overnight, but these are daunting numbers.

The risk-free-rate unfunded obligations are of course worst-case scenarios, relevant only if the funds’ assets earn only the risk-free rate. We should acknowledge, however, that this outcome is entirely possible. In the last 200 years of US stock market history, stocks have performed worse than Treasury bonds for spans as long as 40 years.

Conclusion

My intent is not to stir controversy or to encourage alarm. I am counseling that the pension community would do well to have a few additional facts at the ready, such as the following:

- We should be paying attention to the risk-free rate in addition to knowing the actuarial discount rate (or accounting pension return assumption). Let’s also measure the rate of return required for a pension to be fully funded with current assets. If that is an impossibly high return, then we are well past the point at which we need to be making the tough decisions about how to apportion the pain.

- We already measure the unfunded pension obligations based on the actuarial discount rate. If a pension is underfunded at the actuarial rate of return, then we are tacitly assuming these unfunded obligations will be made up in future years by higher pension contributions, lower payouts, and/or investment returns that are even higher than the (already optimistic) return assumption. We cannot count on the latter, and the politics surrounding lower distributions and higher contributions is fraught, to say the least.

- We should acknowledge the unfunded obligation at the risk-free rate in addition to knowing the unfunded pension obligation. Remember that we are implicitly assuming the capital markets—fund investments—will make up the gap between the unfunded obligation at the risk-free rate and the official unfunded pension obligation. That might not happen. The gains may not materialize.

- Finally, we should know all of these figures on a per capita basis (reflecting the likelihood that taxpayers will be asked to close the gap) and/or on a per employee basis (reflecting the size of the shortfall from the employee’s perspective). This takes the numbers to a human scale so we can viscerally understand the magnitude of the challenges we face.

The COVID-induced crash—notably the crash in interest rates—has boosted the (marked-to-market) unfunded pension obligation for most pension funds by roughly 20% in a single quarter. The lockdown-induced economic crash invites a natural question: If we can’t put Humpty Dumpty back together again in reasonably short order, how will we close an underfunding gap that has been growing for a generation? Can the gap be closed without all stakeholders having a candid conversation about how the pain will be shared? If any stakeholder takes the view that the pain must be borne entirely by others, then the system may well break.

When the plummeting risk-free rate eventually compels actuaries to lower their return assumptions, the official unfunded liability will soar. If (when?) pension fund returns fall short of the actuarial discount rates, the official unfunded liability will soar. The economic reality is that unfunded liabilities have already soared, although this reality is not yet showing up in pension funding reports! Either route it takes, a rise in official unfunded liabilities, for both public and corporate pensions, will almost certainly happen.

Some contend that it is unconstitutional for a state to go bankrupt, and in many states, it is unconstitutional to reduce a pension promise made even decades ago. But no constitution can prevent a state from running out of money or paying with IOUs. Future pensioners deserve better, which requires that we acknowledge the scale of the potential problems and encourage candid conversations among the many stakeholders who expect to fund or to receive these pension benefits.

Better to be forewarned with this kind of knowledge than to ignore it.

Appendix

Please read our disclosures concurrent with this publication: https://www.researchaffiliates.com/legal/disclosures#investment-adviser-disclosure-and-disclaimers.

Endnotes

- My op-eds on the human toll of the lockdown are Arnott (2020) and Arnott and Moore (2020). These represent my personal views. Research Affiliates does not take a view on the wisdom of the lockdown.

- Market dislocation and crisis can provide an extraordinary opportunity to make tactical choices. Buying assets hammered down to implausibly cheap levels at the point of “peak fear,” while trimming assets that are not at all cheap even after the crash can provide an excellent time to invest for the long term (Arnott and Treussard, 2020). Figures are provided in the appendix.

- No investment is truly risk free. In using this terminology, we tacitly ignore the presumably minimal risk of the government directly defaulting on its bonds or indirectly defaulting by deliberately increasing inflation and/or understating the true rate of inflation. Figures are provided in the appendix.

- Duration is a bond market concept with equal relevance in pensions. It relates to the average number of years until bond coupon payments and future principal repayment are to be paid (or average number of years until pension benefits are paid out), weighted by the net present value of those payments. Figures are provided in the appendix.

- Employee wages grow with inflation, typically with an added kicker from real per capita GDP growth, normally around 1%. Until retirement, the TIPS yield plus an inflation assumption is a good discount rate. With the TIPS yield currently negative, the cost of funding these obligations with risk-free assets soars relative to the past. After retirement, pension distributions will grow only in proportion to an inflation component in the benefit formula. Therefore, either the Treasury bond yield or the TIPS yield plus an inflation assumption can be used in some blend to proxy the risk-free rate.

- The source of the figures in the article (unless noted otherwise) is the NASRA (National Association of State Retirement Administrators) website. The appendix summarizes these figrues, which are ostensibly correct as of April 2020. If any are in error, please let us know. Most of the data on assets and liabilities are as of 2018 year-end. We presume that a strong 2019 and a terrible first quarter of 2020 will roughly cancel. The “required return” estimates make simplifying assumptions (e.g., 15-year average duration for pension liabilities) that will lead to imprecision. We estimate about a 1% imprecision (standard error) in the required return numbers and, perhaps, as much as 2% imprecision when they reach double-digits. We believe pension sponsors should know their required return.

- In early 2002, I gave a speech to CIEBA (Committee on Investment of Employee Benefit Assets), a group representing over 100 of the largest corporate pension funds in the country, at their annual meeting. The title of my speech was “Strategic Consequences of Lower Returns.” My main—and very provocative—assertion was that, following the passage of ERISA legislation in 1974 which enshrined the fiduciary rule and the sanctity of pension promises, we had seen a quarter-century of steadily growing importance and influence by the pension community in politics and in the capital markets—and that in the coming quarter-century we would see the abrogation of the pension promise. I made the additional provocative suggestion that defined contribution (DC) plans would not offload all the downside risk onto their employees. Many pension sponsors were using materials that illustrated how the DC plans could fund an employee’s retirement needs based on a typical return assumption of 8%. I opined that the trial bar would turn this into a new “cash crop” for their business.

- Assume New Jersey chose to spend $1,000 less per citizen each year for 20 years and to move these funds into the state’s pension fund. The value of these additional pension contributions, discounted at the risk-free rate, exceeds the $16,013 per resident unfunded liability, but also represents a very big cut in state services to the residents of the state.

- I break out Alaska as a special case, because the state has a very large Permanent Fund based on oil revenues worth nearly $40,000 per state resident. The Permanent Fund roughly matches the state’s unfunded pension obligations, even when those obligations are discounted at the risk-free rate.

- The difference of $4,003 equals a 22% increase from year-end 2018 to March 31, 2020. Given that 2019 was a bull market for pension assets and liabilities, so that the respective changes roughly canceled out, the majority of the 22% increase occurred almost entirely in the first quarter of 2020.

References

Arnott, Robert D. 2004. “Is Our Industry Intellectually Lazy?” Financial Analysts Journal, vol. 60, no. 1 (January/February): 6–8.

———. 2004. “Sustainable Spending in a Lower-Return World.” Financial Analysts Journal, vol. 60, no. 5 (September/October): 6–9.

———. 2015. “Whither Bonds, After the Demographic Dividend?” CFA Institute Conference Proceedings Quarterly, vol. 32, no. 1 (First Quarter).

———. 2020. “COVID-19 and the Unintended Consequences of Economic Shutdown.” RealClear Politics (March 24).

Arnott, Robert D., and Peter L. Bernstein. 2002. “What Risk Premium Is ‘Normal’?” Financial Analysts Journal, vol. 58, no. 2 (March/April):64–85.

Arnott, Robert, and Anne Casscells. 2003. “Demographics and Capital Market Returns.” Financial Analysts Journal, vol. 59, no. 2 (March): 20–29.

Arnott, Robert, and Denis Chaves. 2013. “Mind the (Expectations) Gap: Demographic Trends and GDP.” Research Affiliates Fundamentals (June).

Arnott, Robert, and Stephen Moore. 2020. “Shutdown Is Killing the Economy—and Is Also No Good for Our Health.” TheHill.com (March 25).

Arnott, Robert, and Jonathan Treussard. 2020. “This Too Shall Pass.” Research Affiliates Publications (March).

Garland, James P. 2005. “Long-Duration Trusts and Endowments.” Journal of Portfolio Management, vol. 31, no. 3 (Spring):44–54.

Smith, Vernon. 2020. “The Economy Will Survive the Coronavirus.” Wall Street Journal (April 5).

Wadia, Zorast, Alan Perry, and Charles Clark. 2020. “2020 Corporate Pension Funding Study.” Milliman Corporation (April 28).