Loading...

© 2026 Research Affiliates, LLC. All Rights Reserved.

Key Points

Cyclicality is a feature of both atmospheric conditions and investment performance. The historical record promises that for value investors, summer will follow winter—the challenge is in weathering the passing blizzard of negative returns.

Both U.S. and developed-market RAFI™-based strategies have outperformed their cap-weighted value benchmarks over the long term and on a 1-, 3-, 5-, and 10-year trailing basis.

The largest and most persistent investment opportunity is long-horizon mean reversion, which explains the historical outperformance of RAFI and supports our expectation that the dynamic value tilt of fundamental-index-based strategies will generate future excess returns over the long term.

Both of us are European-born and have a particular appreciation for kitsch-y Americana and its sunny outlook, perhaps as a reaction to our more neutral (some might argue, existential and heavy) cultural heritage.1 High in the firmament of traditional Americana are the “Greetings from” postcards depicting cities and sights from around the United States—although we have noted the enthusiastic adoption of this quaint piece of memorabilia by other locales around the world. The one characteristic shared by all such postcards is the absence of the gloom and grey of winter!

Investors, like all Earth’s creatures, experience “winter”—sometimes as unseasonably long—in asset classes, sectors, strategies, and regions that can stay out of favour for months, years, and even decades. After years of living in Boston, New York City, Paris, and London we can attest that, whereas all four are exciting places to work and live, perfect blue skies and warm sunny days are not permanent features of these cities. While their winters can be unforgivingly harsh and cruelly demoralizing, they are also home to glorious springs, magical summers, and riotously colourful autumns. The same is true in investing. Just as surely as summer follows winter, so too do unpopular strategies and asset classes enjoy their day in the sun.

Investing Seasons

We at Research Affiliates are value investors with a long-term contrarian perspective. We seek securities, asset classes, sectors, and regions that are unloved and undervalued, investing in and overweighting them the more unloved and undervalued they become. Our strategy has a seasonality all its own, just like most reliable sources of long-term excess returns we’ve come across. Although seasons in investing may not conform as neatly to calendars as they do in the physical world, they are undeniably real, with excess returns oscillating between harsh winters and balmy summers.

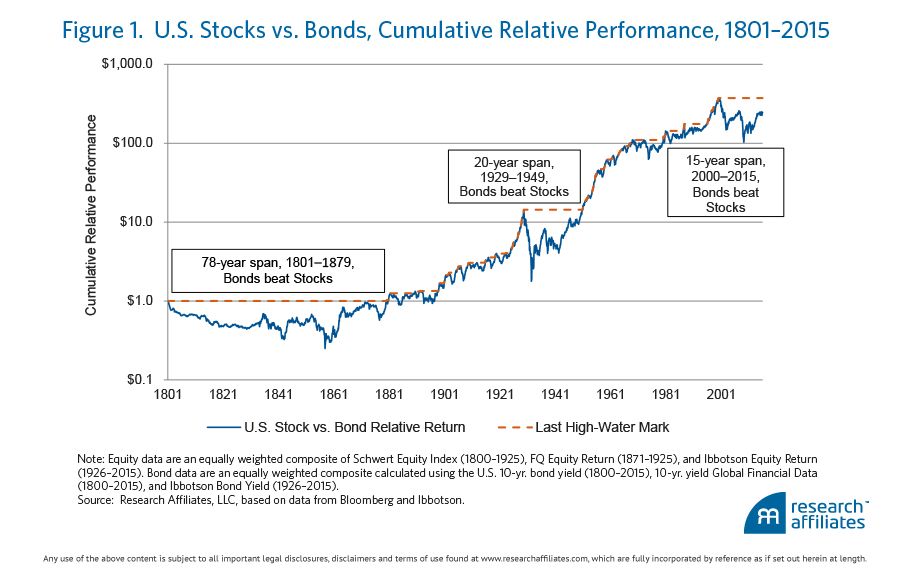

Starting from a broad vantage point, let’s compare the cumulative excess returns of U.S. stocks versus U.S. bonds over the 215 years from 1801 to 2015, as shown in Figure 1. Stocks underperformed bonds for 15 years or more in three instances over this lengthy horizon: a 78-year period comprising most of the 1800s, the 20 years following the Stock Market Crash of 1929, and the last 15 years from 2000 to the present day. Nevertheless, we don’t believe most reasonable investors would argue that abandoning equities entirely as an asset class makes a lot of sense for a diversified long-term portfolio.

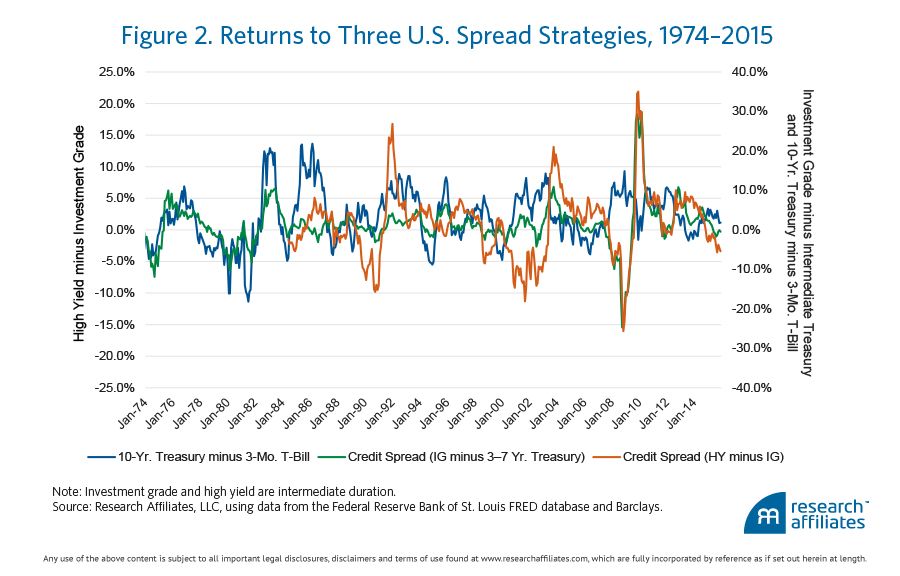

This same seasonality repeats in just about every strategy and sector of the market. Three simple, straightforward spread strategies clearly show the ebb and flow of returns. Figure 2 plots the term premium in U.S. Treasuries (long the 10-year rate and short T-bills) along with two credit spread strategies (long investment-grade credit and short 10-year Treasury, and long high-yield credit and short investment-grade credit). Admittedly crude, and only approximating actual investment strategies, they speak volumes about the functioning of financial markets. All three strategies made good sense over periods as long as multiple decades, accruing returns throughout the entirety of the time series, in no less than 60% of all monthly rolling one-year time windows. Yet notice the cyclicality in returns—even for the innocuous term-premium strategy—with annual reads of plus and minus 10% not being out of the ordinary.

The same pattern is present in equity market strategies, a prime example being value-minded strategies whose cyclicality we’ve described in the past as “unreliably reliable”; thus, in our view, distinguishing between weather and climate is a worthy endeavour. Weather is atmospheric conditions over a short period of time, whereas climate is atmospheric “behaviour” over relatively long periods of time. Cyclicality is an inherent feature of investing (climate), with sometimes volatile swings in returns (weather) over each cycle. But none of this, on the face of it, suggests a strategy is good or bad. It just means staying the course will be more or less uncomfortable. Thus, to assess the intrinsic performance attributes of a strategy requires a long-range perspective.

Using data from the Fama–French online library to examine the ubiquitous HML series (long high book-to-market stocks and short low book-to-market stocks),2 we can illustrate just how long the value “winter” weather has been. But first let’s look at the value “climate.” The mean one-year rolling return since inception of the series in 1926 is nearly 5% and—to be conservative in the face of several extreme realizations to the upside (!)—the median of the series is still an impressive 3.7%. Furthermore, of the 1,063 monthly values for one-year rolling returns, 660 were positive (a “batting average” of more than 60%) despite streaks of negative prints as long as 29 consecutive months.3 In other words, value as defined by HML has been a reliable long-term winner, despite significant short-term disappointment along the way.

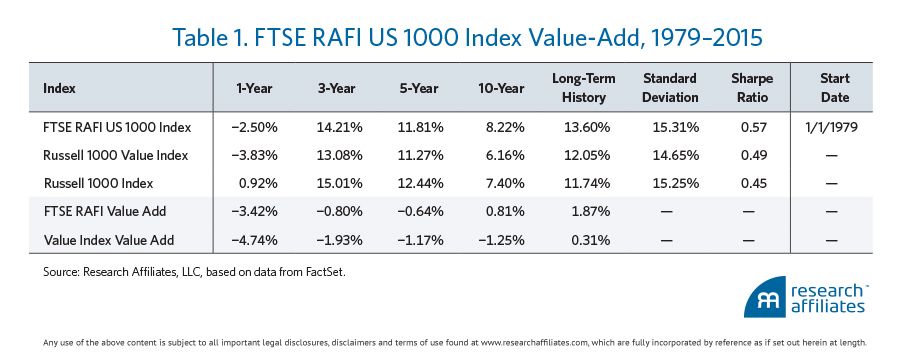

Over the shorter 1979–2015 period (1979 marking the launch of the Russell 1000 Value Index), “plain vanilla” capitalization-weighted value has faced massive headwinds, but in the same environment, fundamentally weighted, value-tilted strategies, such as the RAFI™ Fundamental Index™ series, have withstood the headwinds to generate long-term excess returns. Table 1 compares the performance of the FTSE RAFI™ US 1000 Index and the Russell 1000 Value to the cap-weighted Russell 1000 Index over the 1979–2015 period. FTSE RAFI earned an excess return of 1.87% for the period compared to the 0.31% excess return produced by the Russell 1000 Value.

Let us look more closely at the “seasonality” of a U.S. equity value strategy. In order for a value strategy to generate excess returns, mean reversion in valuations must take place. Simply put, enough “expensive” stocks must get relatively cheaper and enough relatively “cheap” stocks must get at least a little less cheap. But the requirement is not that this happens uniformly and concurrently for every security, just for a sufficient fraction of the market; that said, the last two years or so have been characterised by somewhat extraordinary circumstances in which value has been punished across virtually all sectors on a global scale. In others words, it’s been winter everywhere for the value-oriented investor.

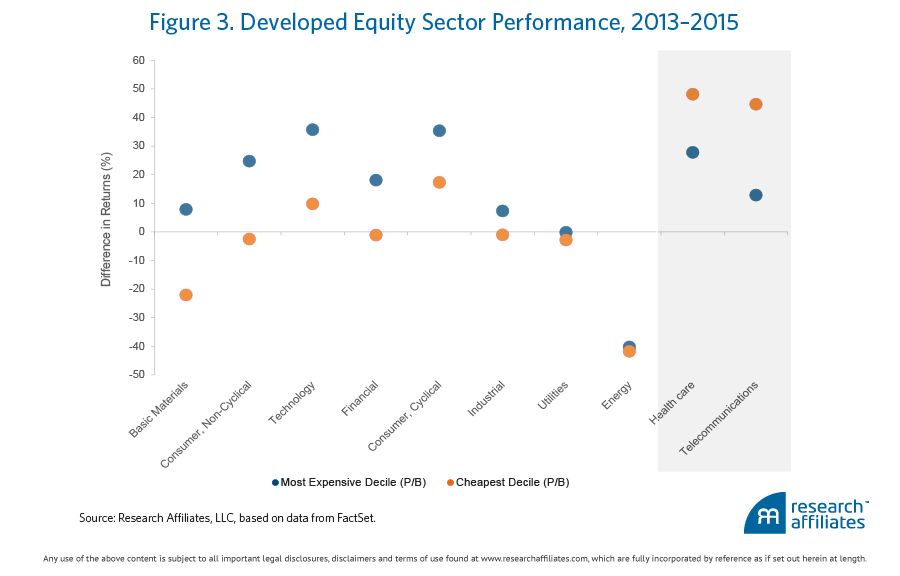

As Figure 3 shows, over the past two years as RAFI-based strategies began to experience significant performance challenges, in nearly every sector of the developed equity market expensive stocks—the top decile by price-to-book (P/B) ratio—beat cheap stocks—the bottom decile. The sole exceptions were the healthcare and telecommunications sectors.

In response to the recurring underperformance of value stocks over the last several years, RAFI-based strategies, relying on a disciplined rebalancing approach, have increased their active weight to the two worst performing developed-market sectors—energy and basic materials—the only two sectors to post negative returns. In 2013, after rebalancing, the active weight to these two sectors for the FTSE RAFI Developed 1000 Index was 2.29%, in 2014 the active weight rose to 3.60%, and in 2015 to 5.59%.

What Winter Looks Like

As if there is doubt in anyone’s mind, let us state unambiguously that we are writing this particular missive from the depths of a very painful winter in value-land. Table 1 shows this clearly. On a 1-, 3-, 5-, and 10-year trailing basis, Russell 1000 Value generated solidly negative excess returns, −4.74%, −1.93%, −1.17%, and −1.25%, respectively. In a parallel, though much milder manner, FTSE RAFI US 1000 posted negative excess returns on a 1-, 3-, and 5-year trailing basis. Last year’s performance was very painful indeed at −3.42%, which dragged down the trailing 3- and 5-year excess returns to near zero.

The long-term tracking error (1962–2015) of FTSE RAFI US 1000 relative to the S&P 500 Index was 4.2% annualised,4 not exactly an “extreme” concentrated deep-value strategy. And yet, pronounced cyclicality is a reality. In the warmest of summers, FTSE RAFI US 1000 may outperform by 20% or greater, as it did in the aftermath of the tech bubble or after the darkest hours of the global financial crisis. Nonetheless, even a 4.2% tracking error allows for deep pain, as exemplified by the negative return posted in 2015.

We must remember, however, that seasons come and seasons go. Eventually long winter nights will give way to seemingly endless summer days in which we can enjoy the ripened fruits of seeds planted much earlier. Our notes then will be sun-filled postcards reporting stupendous excess returns. But summer weeks, like their preceding wintry months, succumb to the passage of time—and anchoring on their lost splendour only makes the next winter that much more difficult to tolerate.

Global Winter—Not Just the Northern Hemisphere

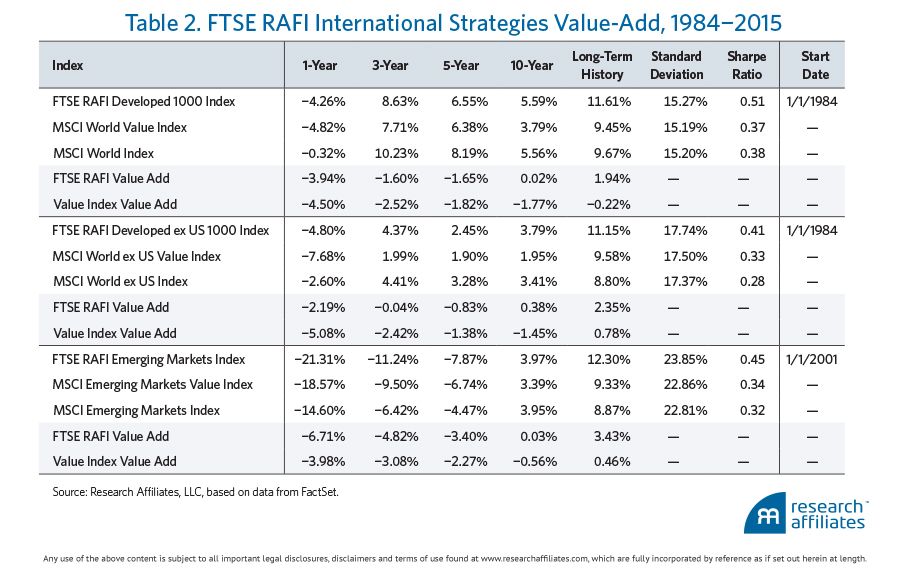

The same performance pattern for value relative to cap-weighted indices realised over the last decade in the United States also holds for similar strategies beyond the United States. In the long term, RAFI-based international strategies produced meaningful value-add, outpacing cap-weighted benchmarks by 1.94% (developed equities), 2.35% (developed equities ex U.S.), and 3.43% (emerging markets), as reported in Table 2. Shorter-term horizons, however, reveal a different story.

For the three years ending December 2015, the FTSE RAFI Developed 1000 ex US Index underperformed the cap-weighted MSCI World ex US Index by a handful of basis points (−0.04%); by comparison, the MSCI World ex US Value Index underperformed by −2.42%. Over the same period, in emerging markets, where value has been most severely punished, the RAFI strategy more pronouncedly underperformed, down −4.82% versus the MSCI Emerging Markets Value Index underperformance of −3.08%, both relative to the cap-weighted benchmark. Indeed, the winter in value-land is being felt around the globe.

Last-Minute Winter Getaways

The long and unforgiving winter in value-land has left many investors understandably craving a little sunshine. We’ve been there—caught in the grip of a steely grey winter—desperately jumping on the internet to book a last-minute flight to an island paradise for a couple of days, only to return tired and poorer. Much like last-minute tickets to the Caribbean or Mediterranean have a nasty habit of being extremely expensive in the darkest days of February, the getaways available to investors seeking relief from their recent experience in value strategies may prove expensive and disappointing.

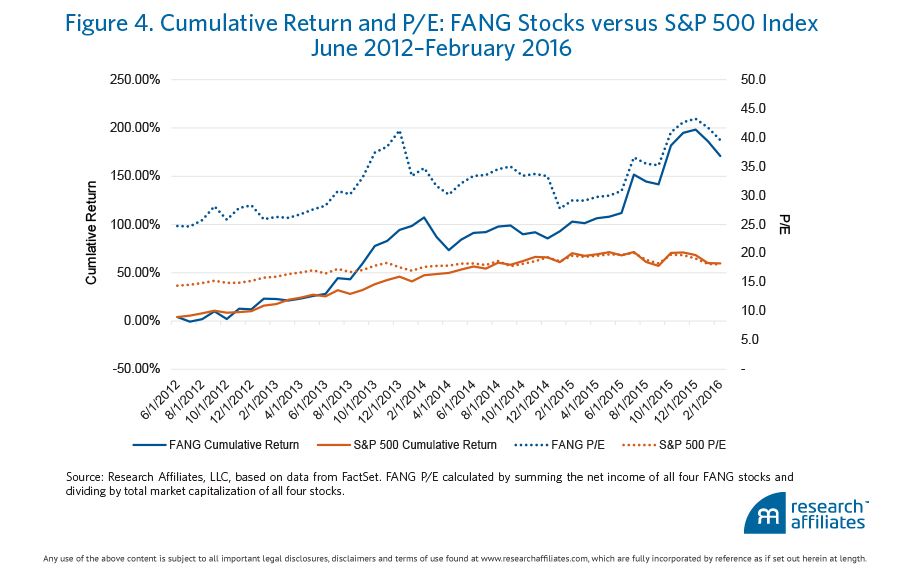

Consider the market darlings known by their acronym FANG5 (Facebook, Amazon, Netflix and Google, now Alphabet). Collectively, as illustrated in Figure 4, the stock prices of these four companies increased 200% from June 2012 to year-end 2015. In addition, the collective P/E of the four nearly doubled over the same period, indicating their stupendous returns are largely a result of their becoming more expensive, much like the cost of that last minute trip! The rise in the FANG stocks’ collective P/E is of particular note when compared to the P/E of the S&P 500 at year-end—approximately 42 vs. 20. For a few days in early February 2016, Google overtook Apple in terms of market capitalization, a dubious honour and not an encouraging sign for investors jumping into Google after such a run-up. This move, of course, isn’t all that has occurred in the early weeks of 2016. The market has seriously corrected, taking with it the prices of the FANG stocks, very possibly an early crack in growth stocks’ running the table.

Another perspective on cyclicality is a recent study by Arnott et al. (2016) that examines six common U.S. equity strategies—value, positive momentum, small cap, illiquid, low beta, and high gross profitability—since 1967. A comparison of the relative valuation and subsequent relative performance for each indicates a strong link between the two: the market’s performance-chasing behaviour has created much of the factor’s return. This rise in relative valuation not only boosts past relative performance, it also opens the door for subsequent lower returns when valuations revert to historical norms. In fact, seeking a “return”-getaway in any of the five strategies (other than value) analysed in the study appears to invite an expensive one-way ticket to underperformance when valuations inevitably adjust.

Restorative Summer Holidays

Similar to the angst experienced by blizzard-trapped and drizzle-logged denizens of frozen and bitter climes, the pain felt by value investors is tangible. In the midst of the dreariest days, it’s all too easy to overlook the fact that these exact conditions presage a reversal in seasons and will eventually usher in a possibly extended span of strong returns for disciplined value investors. Mean reversion has shown itself to be a reliable and powerful force, and the most persistent investment opportunity for long-term investors.

Could we attempt to assess the “turn” in the weather by relying on our observations of past and current signals? Of course, but past is not prologue. Rather, we are taking shelter from the adverse elements in a disciplined value-oriented strategy. A boon of fundamental index–based strategies is their persistent ratchet-like moves to a deeper value posture whenever value rotates out of favour or further out of favour. Then, when the inevitable snap-back in mean reversion occurs, these strategies should recover significantly more than the losses they endured during the value winter. As time and experience has repeatedly proven, disciplined value investors, such as ourselves, will be rewarded—one day (we hope soon!) to be basking in long-awaited summer breezes.

We would like to believe that the first few weeks of 2016 are the beginning of the winter thaw, as expensive, growth stocks come under pressure. Are we experiencing an inflection point? Are summer days just ahead? Only time will tell. But we are confident enough in the coming warmer weather that we are perusing the book stand to choose our beach reading list and searching the attic to locate our luggage under the eaves.

Endnotes

This positive outlook may very well be why we both work for an American enterprise, and one of us made a home in the United States more than half a lifetime ago.

This exceptionally long episode (29 months) of poor performance in value stocks extended from September 1989 to January of 1992; the recent rut for value, according to the same data series, is in its 15th month.

Other FTSE RAFI Index strategies have exhibited annualised tracking error in the 4–6% range over the 1962−2015 period.

Being included in an acronym seems to be a highly contrarian indicator, at least based on the appearance of the now disgraced BRIC countries: Brazil, Russia, India, and China. These four nations went from beacons of hope to toxic waste in the eyes of global investors shortly after reaching acronym status. Keenly aware of the exaggerated mood swings of market participants, we trust the truth is somewhere in the middle—neither beacons of hope nor toxic waste.

References

Arnott, Robert D., Noah Beck, Vitali Kalesnik, and John West. 2016. “How Can ‘Smart Beta’ Go Horribly Wrong?” Research Affiliates Fundamentals (February).

Brightman, Chris, Jonathan Treussard, and Jim Masturzo. 2014. “Our Investment Beliefs.” Research Affiliates Fundamentals (October).

Hsu, Jason, Brett W. Myers, and Ryan Whitby. 2016. “Timing Poorly: A Guide to Generating Poor Returns While Investing in Successful Strategies.” Journal of Portfolio Management, vol. 42, no. 2 (Winter):90–98.