Loading...

© 2026 Research Affiliates, LLC. All Rights Reserved.

Key Points

We believe the Federal Reserve is overstating the importance of falling inflation expectations, which have become disconnected from the Fed’s target and shown to be poor predictors of CPI inflation.

We propose a bottom-up approach to forecasting that is independent of the expectation proxies. Our approach suggests that inflation will reach the 2% target by year-end 2016, a significantly higher forecast than what is currently expected by swap and TIPS markets.

Deflationary risks in the United States are minimal, and investors should anticipate that the Fed will achieve its inflation target sooner than otherwise suggested.

U.S. Federal Reserve officials have expressed concerns about falling inflation expectations, which according to their models should lead to a higher deflationary risk. Indeed, the macroeconomic models favored by the central bankers identify inflation expectations as a key driver of price dynamics and, as such, expectations have become a major target of monetary policy. Recent research suggests, however, the American public has little knowledge of the Fed and its policy goals. Fortunately, we do not find this cause for despair: precisely for this reason—that is, the disconnect between the American public and the Fed—we believe central bank officials should not be concerned about falling consumer inflation expectations, and calls for renewed monetary easing are unwarranted.

The Fed: Who?

The U.S. Federal Reserve is probably the most scrutinized and carefully followed institution in the financial industry. Yet, this popularity is in stark contrast with reality for most U.S. households, as explained in a paper recently presented at the American Economic Association meetings in San Francisco. Macroeconomist Yuriy Gorodnichenko and his coauthors (Kumar et al., 2015) document that the American public is largely unaware of the Fed and its leadership. Recent household surveys show that only about one-third of respondents could identify Janet Yellen as the chairwoman of the Fed, even when given her name as one of four possible choices. In addition, the respondents had difficulty accurately describing recent inflation dynamics as well as providing confident long-term forecasts, thus highlighting the divide between the U.S. monetary authority and the public.

As a Fed official, facing the reality of obscurity in the contemporary American experience must be heartbreaking. Since 2012, the Fed has been explicitly communicating its long-term inflation target of 2% in an effort to influence and direct public expectations. The Fed greatly relies on this policy tool to maintain “firmly anchored” expectations, which are viewed as a requisite means of avoiding potential deflationary and inflationary pressures such as those experienced, respectively, in Japan over the last 20 years and in the United States in the 1970s.

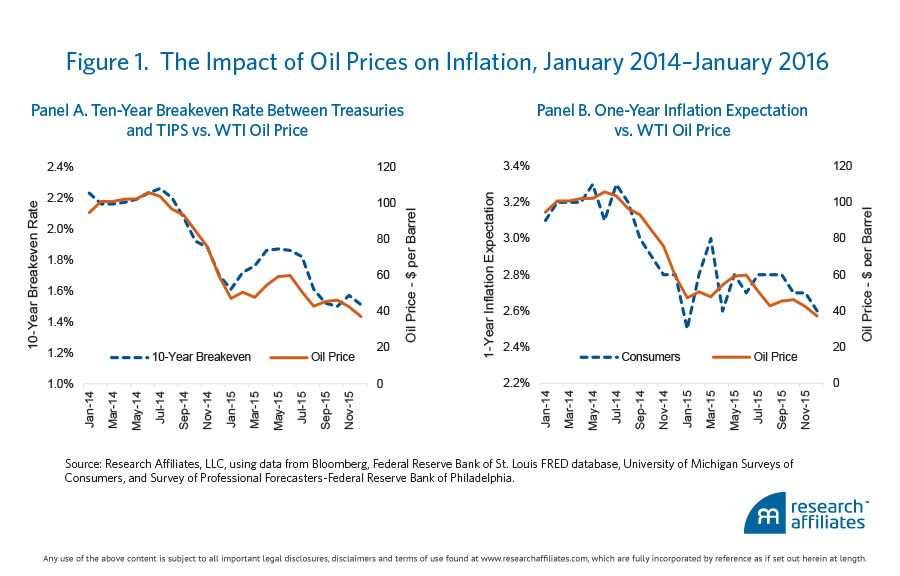

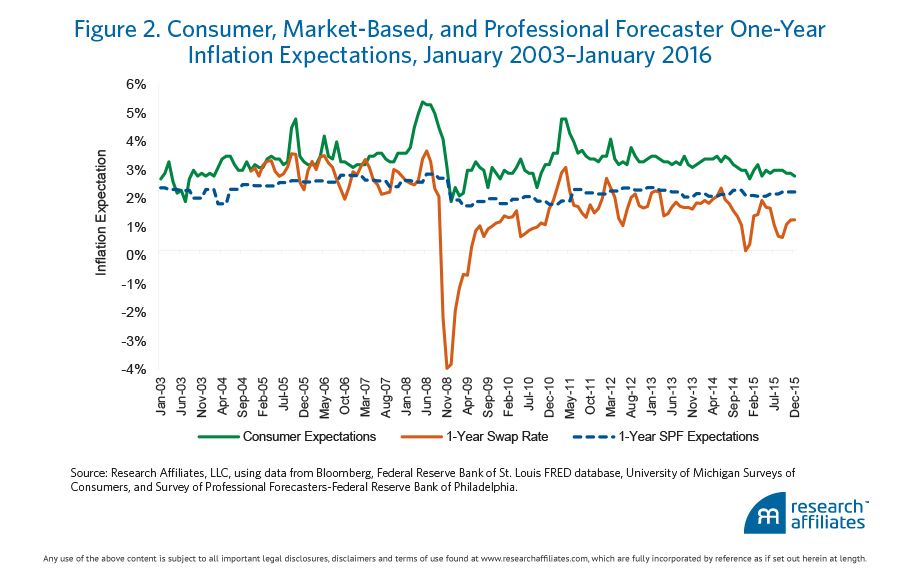

Officials, such as New York Fed President William Dudley (2016), are beginning to express concerns regarding the risk of expectations becoming unanchored with the continued fall in energy prices. Although the influence of the price of oil on inflation is known to be generally transitory in nature, some officials are concerned that a sustained fall in energy prices might lead to deflationary pressure. As Figure 1 shows, falling energy prices have depressed both market-based and consumer expectations about inflation at different horizons, a dynamic that could gain speed if consumers postpone purchases and businesses delay new investments.

The combination of low energy prices and a “low-visibility” central bank could increase investor uncertainty about both short-term and long-term U.S inflation rates. While the Fed worries about inflation expectations, the public pays little attention to the Fed’s goals and focuses on those items directly related to their daily experience, such as commuting costs. In our view, the Fed has no need to worry at the moment about the public’s expectations. Indeed, consumer and market-based forecasts have been inferior predictors of future inflation, a fact sufficient to cast doubt on the models evoked by some Fed officials.1

Unaligned Expectations

The theoretical rational behind the Fed’s interest in influencing inflation expectations is the expectations-augmented Phillips curve, or New-Keynesian Phillips curve, which links the realized inflation rate to expectations as well as to measures of real economic activity, such as the unemployment rate or the output gap. But although the modern Phillips curve provides an important theoretical benchmark, its empirical robustness is still debated.

Ideally, the Phillips curve’s expectation proxy would be a measure of firms’ inflation expectations; unfortunately, no such statistic exists and we must rely on another proxy. Three common proxies are plotted in Figure 2: the one-year-ahead inflation forecasts of consumers, financial markets, and professional forecasters. The differences among these series are substantial. In recent years, consumers’ expectations have been systematically higher than other forecasts and actual inflation. In addition, consumer and market-based expectations have been significantly more volatile—suggestive of a higher correlation with oil prices—than those of professional forecasters; hence, using the Phillips curve to model inflation can result in drastically different forecasts depending on the choice of expectations proxy.

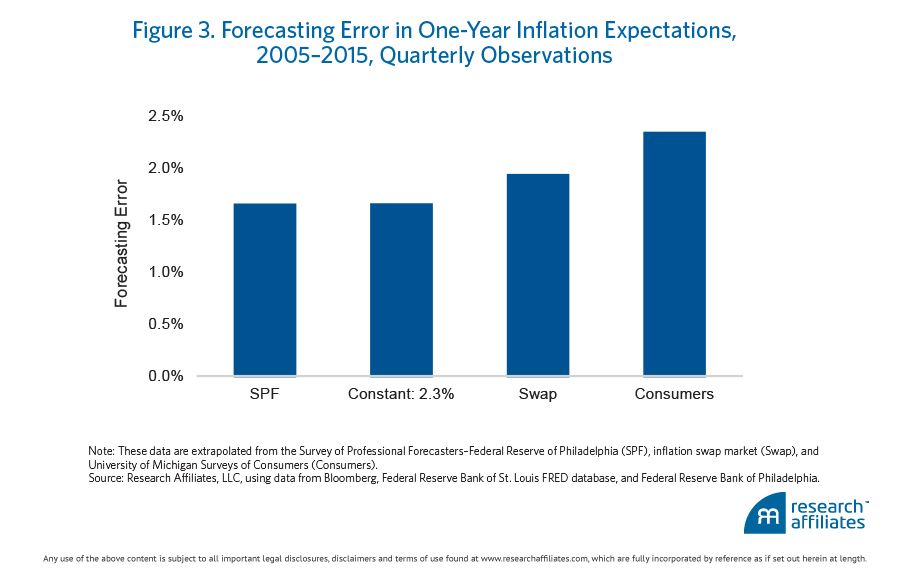

We can judge the accuracy of the various proxies by comparing their forecasting errors, reported in Figure 3. We calculate the forecasting error (i.e., the root of the average squared forecast errors) over the 10-year period 2005–2015 for four measures: a constant 2.3%, which is close to the Fed’s inflation target, and forecasts from professional forecasters, consumers, and swap markets.2 The Fed targets the personal consumption expenditure price index (PCEPI), which over the last 15 years has tracked about 0.3% lower than the Consumer Price Index (CPI), also known as headline inflation. We focus on headline inflation forecasts in this article; hence, the selection of our constant, 2.3%.

Between 2005 and 2015, consumer and market-based expectations were the least accurate predictors of subsequent year-over-year inflation. As documented by Bauer and McCarthy (2015), inflation swap contracts performed poorly compared to professional forecasters and to the constant. Consumer expectations constituted a particularly noisy signal versus other metrics. Indeed, over the last few years, consumers have systematically overestimated future inflation by about 1.2%. As suggested by Kumar et al. (2015), factors such as the price of gas at the pump and the prices paid in the shops have a great influence in shaping public perception—much greater than the messaging of the Fed.

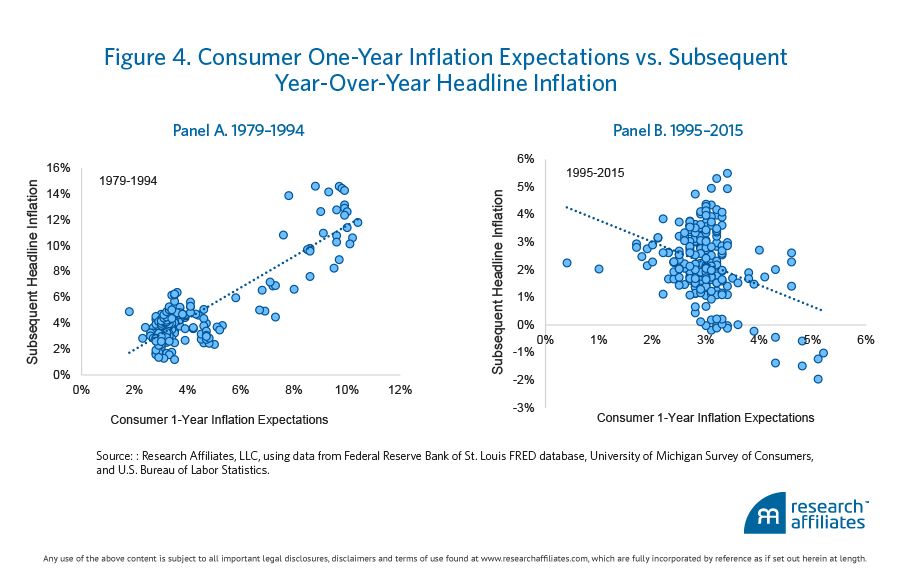

Ultimately, the economic importance of consumer expectations depends on their underlying driving force. To better understand the factors influencing consumer inflation expectations in recent years, we contrast in Figure 4 the one-year inflation expectation, based on the University of Michigan Surveys of Consumers, with the subsequent realized one-year headline inflation rate for two historical periods: 1979–1994 in Panel A and 1995–2015 in Panel B. The earlier period is characterized by core and headline inflation rates dramatically falling after Paul Volcker took the helm at the Fed. The latter period is characterized by the so-called Great Moderation and the financial crisis, years in which inflation has been roughly stationary.

The positive relationship illustrated in Panel A over the 15 years from 1979 to 1994 suggests that during this period households inherently understood changes in trend inflation (i.e., their forecasts shifted downward in tandem with generalized inflation). In contrast, Panel B shows a negative correlation between one-year inflation expectations and subsequent year-over-year headline inflation during the 20-year period 1995–2015. This negative relationship is a product of the oil price dynamics during the financial recession. Over this period, households appear to have assigned a particularly large importance to energy price variations that turned out to hold little information about subsequent inflation. Households likely misunderstood the transitory nature of oil price fluctuations, a situation we might be witnessing again today. Market-based expectations show the same sort of bias, although the causes are less clear and at least partially related to the microstructure of the financial markets.

A Simple Alternative to Inflation Expectations

Given the practical ambiguities in modeling inflation using the Phillips curve, an alternative is to separately analyze each component of CPI. Our approach allows a large degree of modeling heterogeneity across the prices of different goods and services without requiring an explanation of the dynamics within a unique framework.

To use this approach, we disaggregate core inflation from headline inflation, isolating the more volatile CPI subindices of food and energy, which currently represent about 14% and 7%, respectively, of the headline index. Oil’s collapse from about $105 a barrel in mid-2014 to approximately $35 in early March 2016 has been the predominant driver of energy inflation, which fell almost 13% over 2015. Given its importance in the aggregate index, this drop translates into about a full percentage point being subtracted from headline inflation. Food inflation has also been below average, partially due to a strengthening U.S. dollar and cheaper oil, the latter implying, among other things, lower transportation and packaging costs.

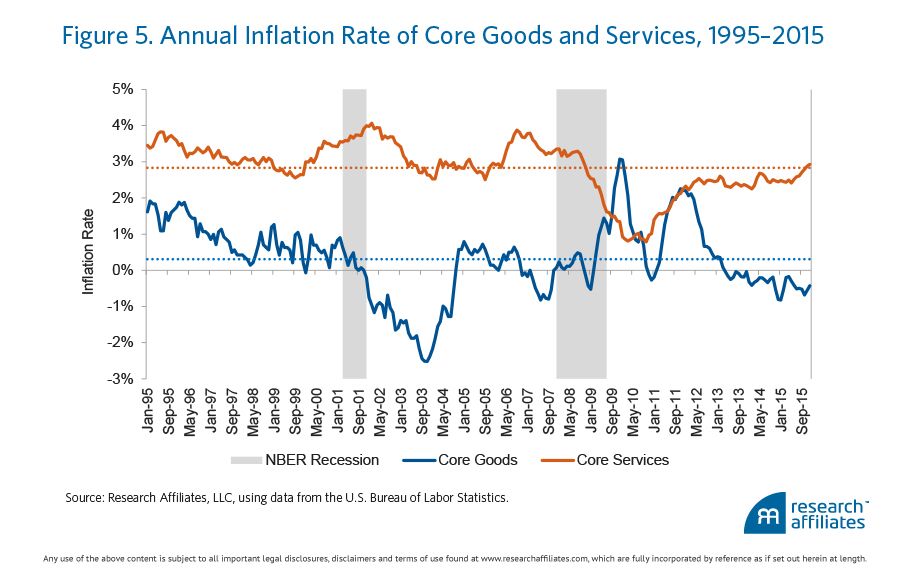

The annual inflation rate of core goods and services, which account for about 19% and 59%, respectively, of headline CPI, offer a blurrier picture, as Figure 5 illustrates. Different dynamics impact these two indices. Goods inflation is closely related to the global economy and to the path of the U.S. dollar because globalization has led to greater foreign competition for U.S. manufacturers. In contrast, services inflation is closely related to the housing market and to the national economy, characterized by lower substitutability of the labor force.

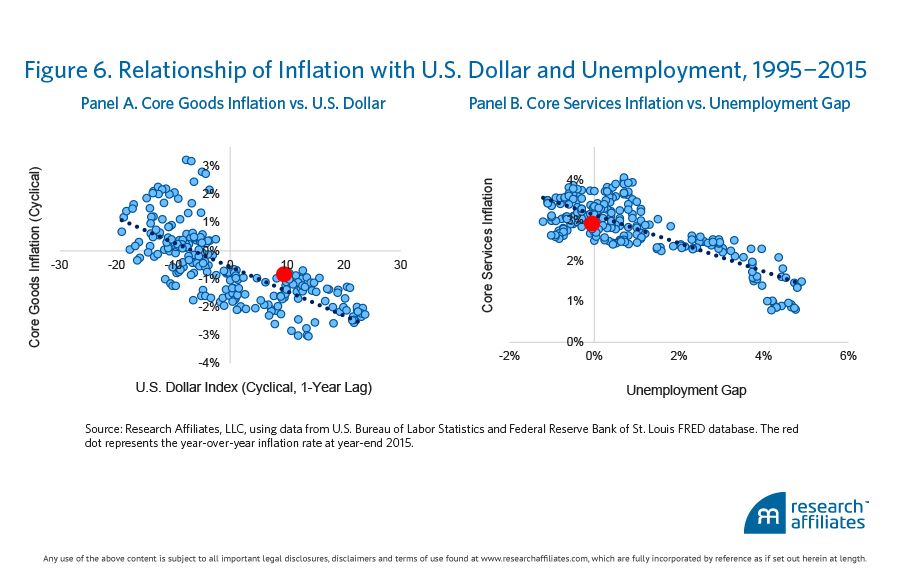

The macroeconomic relationships between goods inflation and the U.S. dollar, and services inflation and the unemployment gap, are captured in Figure 6. Panel A points to a significant negative relationship between the real exchange rate of the U.S. dollar (trade-weighted against the major currencies) and subsequent goods inflation. Both variables are expressed in cyclical terms (i.e., as differences with respect to their 10-year trailing averages). The dollar index is lagged by one year because its effect tends to be felt gradually over time. A year ago, the U.S. dollar exchange rate stood 11% above its 10-year trend versus other major currencies, indicating goods inflation would likely fall by 0.3% in 2015. Realized goods inflation in 2015 was, in fact, −0.4%; hence, a strong dollar has contributed to subpar goods inflation, a phenomenon American consumers should welcome.

Panel B expresses a similarly powerful relationship between services inflation and the current unemployment gap, defined as the difference between the equilibrium unemployment rate (estimated by the Congressional Budget Office) and the actual rate. A shrinking gap is associated with greater demand for housing and with higher wage pressure, both of which act as tailwinds to services inflation. Today’s unemployment gap indicates that services inflation over the past year should have been 3.2%. Here too the expectation was largely in line with what transpired; services inflation rose by 2.9% in 2015. In light of these relationships and the most recent macroeconomic data, the latest readings of the inflation data are not surprising. In 2015, core inflation was 2.1%, just 0.2% less than what would be anticipated based on Figure 6. Inflation rates are consistent with the historical experience, which indicates we are far from witnessing a major structural break within the U.S. economy.

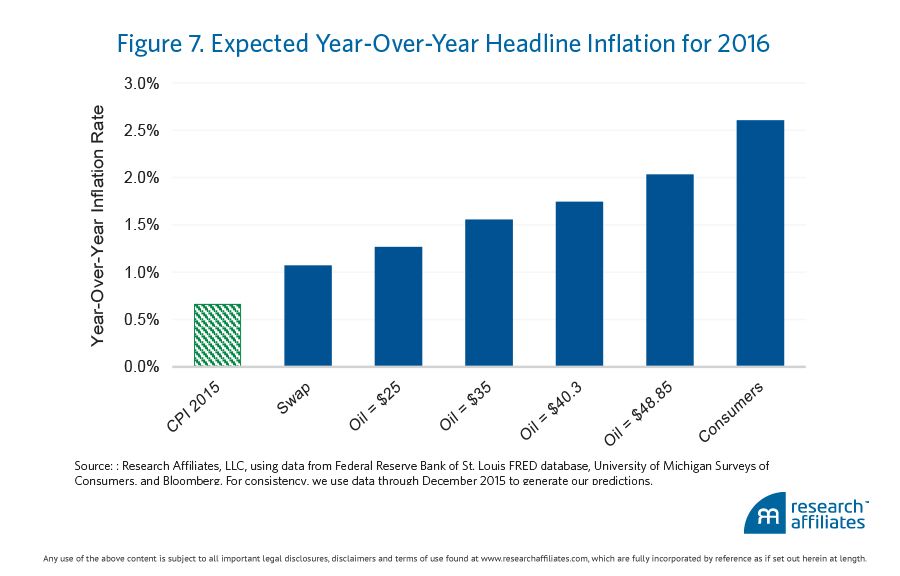

By leveraging this analytical framework, we can compare alternative inflation forecasts for 2016, each associated with a different expected oil price. We employ a simple reduced-form forecasting model, which builds on the relationship highlighted in Figure 6,3 to analyze how headline inflation is likely to evolve if the price of oil should gradually converge in December 2016 to $25.00, $35.00, $40.30, or $48.85 a barrel. A $25.00 price would indicate extended weakness in the global economy, a $35.00 price would represent essentially no change from the current price level, and a price of $40.30 would correspond to the expectation extrapolated from the futures market. A $48.85 price would reflect the median analyst forecast from the survey compiled by Bloomberg.4

The 2016 year-end inflation forecasts derived from the four oil price scenarios are shown in Figure 7.5 In addition, we include 1) the 2015 headline inflation rate, 2) the market’s one-year-ahead expectation at 2015 year-end based on the swap rate, and 3) the forecast from the University of Michigan Surveys of Consumers. Should the price of oil rebound to $48.85 as expected by analysts, we predict 2016 CPI inflation to be around 2%, just short of the Fed’s target. If oil prices remain subdued in the $25.00 to $30.00 range, year-over-year inflation will likely stabilize around 1%, then move higher toward year-end. In contrast, both the inflation swap market and consumers are forecasting an inflation rate outside the range forecasted by reasonable oil price estimates. Once again, the evidence suggests that both consumer and market expectations may be of minimal help in navigating inflation dynamics.

Monetary Policy Still on Target

Despite its best efforts, the U.S. Federal Reserve has failed to earn the full attention of the American public. But this is exactly the reason Fed officials should not be concerned about falling consumer and market-based inflation expectations. Today’s situation is different from that of the 1980s when core inflation dramatically fell from a double-digit peak. Current expectations appear to be mostly influenced by transitory fluctuations in the price of oil. As such, estimating the modern Phillips curve has the flavor of an academic exercise, providing marginal practical insights compared to a more elastic bottom-up view of the inflation index. Should the oil price match analysts’ year-over-year expectations for December 2016, we predict headline inflation to gradually reach the 2% mark by the end of the year, close to the Fed’s target. Monetary policy might be unpopular and confusing, but it is not broken. Investors should be prepared for the Fed to reach its inflation target sooner than what is suggested by popular indicators.

Endnotes

For another example, see Oil's Impact on Inflation Really Is Transitory (With One Caveat).

Like Bauer and McCarthy (2015), we exclusively investigate the end of the first month of each quarter because this is the time the Survey of Professional Forecasters–Federal Reserve of Philadelphia (SPF) predictions are formulated; the SPF frequency is quarterly.

We model the following relationships: 1) energy CPI, a function of oil prices; 2) food CPI, a function of lagged energy CPI; 3) core services CPI, a function of the unemployment gap; and 4) core goods CPI, a function of cyclical fluctuations in the level of the U.S. dollar. For simplicity, we assume unemployment and the U.S. dollar will remain at recent levels; moderate fluctuations in these two variables have only a marginal impact if compared to potential fluctuations in energy prices.

The $48.85 price constitutes the median analyst forecast for the average crude WTI Nymex oil price at year-end 2016. The forecasts were made in January 2016.

We use inflation data through December 2015 to generate our predictions. The recent gyrations in the oil market do not change the core message of our analysis.

References

Bauer, Michael D., and Erin McCarthy. 2015. “Can We Rely on Market-Based Inflation Forecasts?” Federal Reserve Bank of San Francisco Economic Letter 2015-30.

Dudley, William C. 2016. “The U.S. Economic Outlook and Implications for Monetary Policy.” Remarks at the Economic Leadership Forum, Somerset, New Jersey, January 15.

Kumar, Saten, Hassan Afrouzi, Olivier Coibion, and Yuriy Gorodnichenko. 2015. “Inflation Targeting Does Not Anchor Inflation Expectations: Evidence from Firms in New Zealand.” Brookings Papers on Economic Activity, presented at Fall 2015 Conference.

Surveys of Consumers, University of Michigan, University of Michigan: Inflation Expectation© [MICH], retrieved from Federal Reserve Bank of St. Louis FRED database.