Uncomfortably Stuck Between Past and Future: Rates, Credit, and Alternative Bond Indices

Strategies that emphasize the bonds of countries with strong debt-servicing economic resources, rather than the bonds of countries with the highest debt issuance, have the potential to outperform.

High-yield index strategies, which mirror factor investing in equities, especially the intersection of quality and value, offer investors the opportunity to outperform traditional high-yield indices.

In today’s low-yield environment, investors with fixed income mandates can improve performance with strategies designed to pick up incremental returns from mean reversion and that limit overexposure to both lower-quality creditors and large issuers.

As investors, we are constantly in the uncomfortable position of having to plan for the future with limited guidance from the past. Our job byline may as well be “uncomfortably stuck between past and future.” As a striking example, the relentless global march toward lower bond yields over the last 40 years is rather unlikely to persist in the decades to come. As zero to negative interest rates take hold around the world, many of the principles we use to navigate capital markets become increasingly less valuable (Brightman, 2016). The concept of a risk-free return, as a result, is teetering on the edge of relevance these days—quaintly unhelpful at best, wealth-destroying at worst.

Investors whose mandates include fixed-income allocations face some difficult decisions. Strategies designed to pick up incremental returns from mean reversion and that limit overexposure to both lower-quality creditors and large issuers have the potential to deliver a welcome edge in performance to both government and high-yield bond investors.

Bonds in Current Time

Although government bonds may provide investors near certainty of notional capital being returned, the risk of locking in long-term losses can also be a near certainty with negative real rates and the prospect of interest rates inevitably trending higher. Equating risk and volatility may be too simplistic to deal with the world we face today. In markets for government debt, favoring the a priori safe bet of high-debt-issuer countries, such as the United States, Japan, and developed European nations, can be far riskier to an investor’s wealth than interest-rate volatility or credit ratings may suggest. And although volatility can be an investor’s friend in credit markets, especially in high-yield corporates, by creating opportunities to trade against short-term mispricings, not all risk-taking is rewarded equally.

Improving Government Bond Portfolio Returns

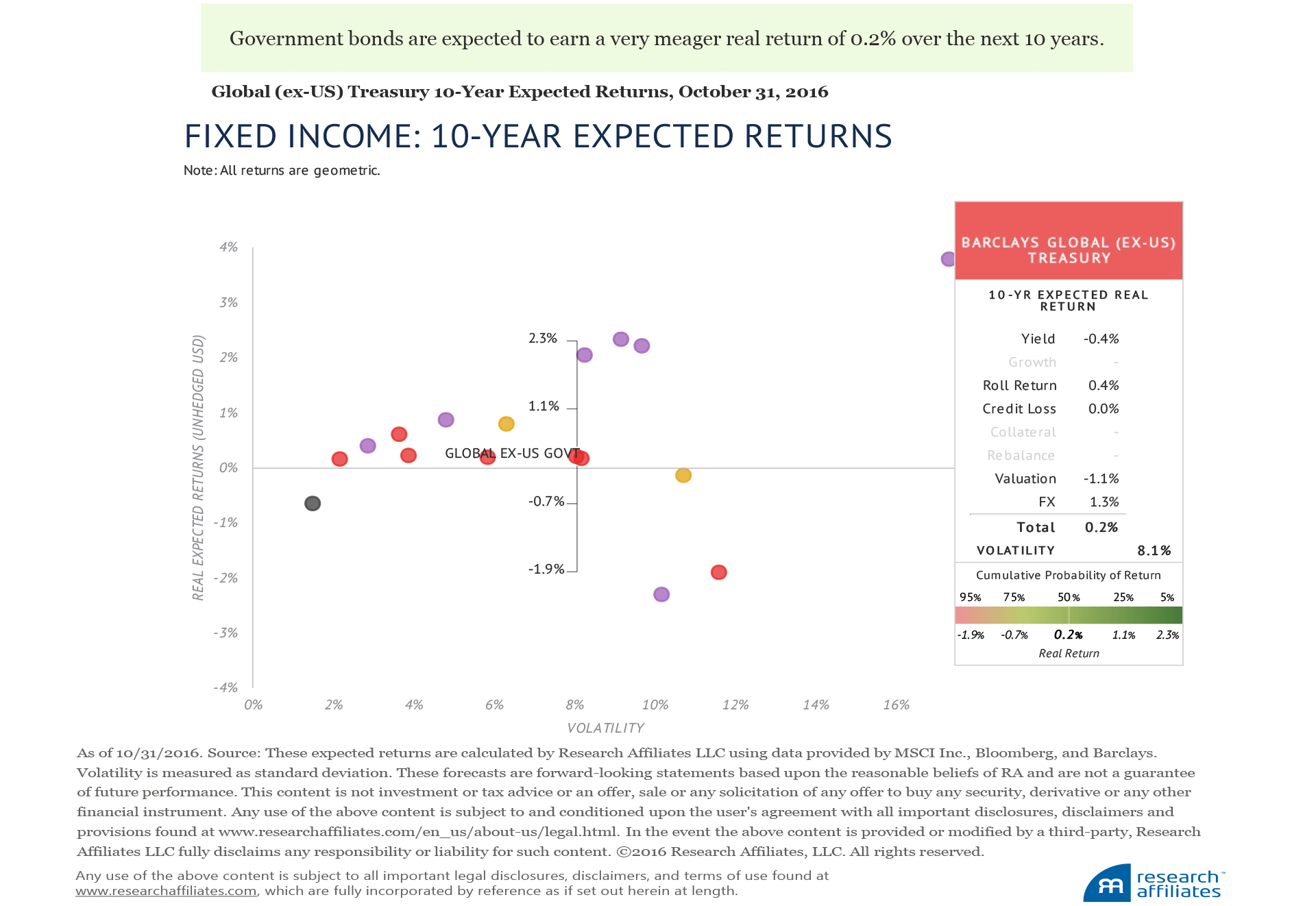

A simple, yet robust, framework for forming reasonable long-term expectations is offered in the Research Affiliates expected returns methodology, publicly available on our website. As of October 31, 2016, our methodology suggests that global (ex-US) Treasury markets, measured by the Barclays Global (ex-US) Treasury Index, are expected to return between −1.9% and 2.3% over the next decade, with a central tendency of 0.2%, after inflation. The fact that the central tendency is positive is largely the result of expected currency movements. A weakening of the US dollar relative to global currencies is expected to add 1.3%, but no help is offered from the current real yield of −0.4% and the −1.1% expected return from current high valuations.

For many investors, an allocation to government bonds is the starting point for portfolio construction. When that allocation is expected to return nearly nothing over the next 10 years, the task of constructing a satisfactory portfolio is just that much more challenging. That said, a likely path for improving long-term potential returns in global government bonds is to be thoughtful and disciplined in allocating to country exposures.

Bond markets are built on the premise that issuers can borrow against the future, and some countries seem to be borrowing from a future far less rosy than thorny. With both high starting debt burdens and demographic trends associated with significant off-balance-sheet future borrowings combined with a reduced ability to spur growth, advanced economies such as Japan and the United States face major impediments to managing their ballooning national debt burden in the future. Yet, the debt of these countries dominates government allocations in traditional bond indices as a mechanical byproduct of their dominance in cumulative notional issuance.

Over the last few years, investors have been rewarded for their substantial exposure to these countries. A combination of bond-buying programs by central banks, negative- and zero-interest-rate policies, and continued fears that a new global crisis may be around the corner (a hard path to Brexit being the latest source of such concern) have held the pedal down on the flight to safety. Perhaps conditions will remain in place for investors to benefit from these allocations, but the possibility for retrenchment can also be convincingly argued: bond markets allow creditors to borrow against the future, and eventually the future tends to conform to harsh (but logical) economic realities, not feel-good hopes and fictions.1

Investment professionals are familiar with the saying “don’t fight the Fed.” While this may aptly apply to traders, long-term investors can be less heedful of this admonition. Those with long-term investment horizons can benefit by gaining exposure to bond strategies that allocate to countries on the basis of debt-servicing economic resources rather than debt issuance, effectively raising the relative credit quality of holdings. Gaining exposure to the less popular, less prolific issuers, not widely viewed as safe harbors in a volatile world, also allows long-term investors to capitalize on market inefficiencies.

Investors who position their portfolios to benefit from the reassertion of long-term economic realities may not find it comfortable or profitable in the short term. For instance, in the year ending September 30, 2016, the Citi RAFI Sovereign Developed Market Bond Index, an index that anchors on fundamental measures of a country’s size relative to the world economy, underperformed an issuance-weighted index by approximately 1.5%. The underperformance was driven by a substantial underweight to Japanese debt just when the country was experiencing an extraordinary bond rally engineered by the Bank of Japan’s quantitative easing program.2 The average weight to Japan in the fundamentally weighted index was roughly 9% versus 30% in the cap-weighted index over the 12-month period.

We would not expect the recent underperformance to continue indefinitely, but neither can we predict when the tide will turn in favor of fundamentally weighted developed sovereign bond indices.3 Investors, for example, who have taken the position that Japan’s interest rates will imminently reverse (after a protracted 20 years or more hovering at zero or just above) have entered into a trade notoriously known as “the widow maker.” Our preference would be to protect our families from such a fate.

In global government bond markets today, investors seem to be standing atop tectonic plates, which are moving slowly yet predictably, defying simple rules of thumb about risk-free investing, and rendering the last 40 years of historical data a very poor guide for making decisions about the future. In the current vacuum of relevant historical experience, investors who choose a strategy that follows a rules-based methodology which emphasizes debt-service capacity, capitalizes on observable inefficiencies, and implements at low cost, should be well-positioned to weather the era-defining changes likely ahead.

Improving High-Yield Bond Portfolio Returns

Investors in corporate credit, especially high-yield bonds, tend to face shorter cycles of booms and busts than do government bond investors, and therefore have more frequent opportunities, as a result of year-over-year price volatility, to advantageously position their portfolios. High-yield bonds are an equity-like asset class, whose returns are overwhelmingly driven by credit spreads and credit losses, not rates and duration.

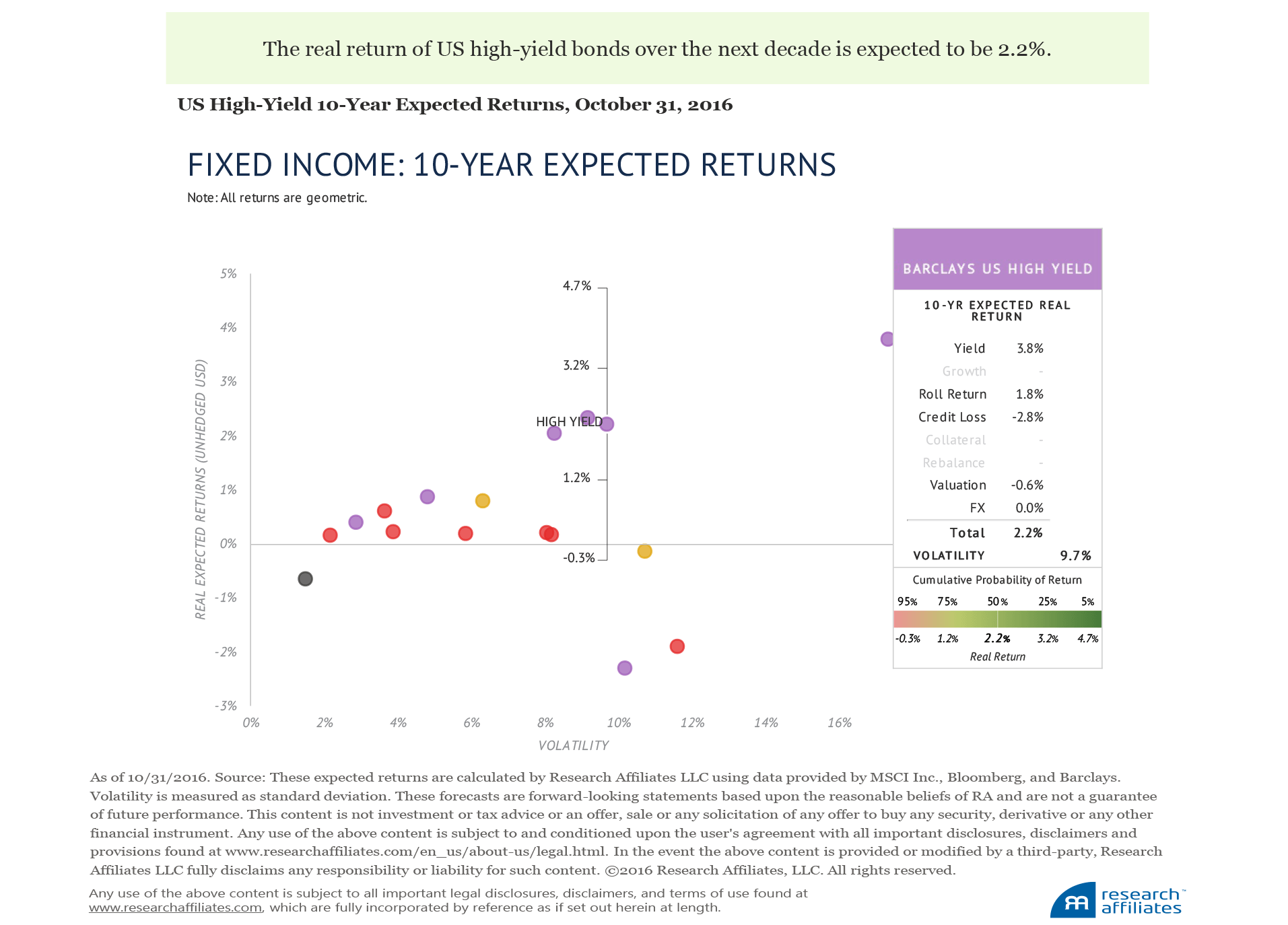

The Research Affiliates expected returns methodology suggests that, as of October 31, 2016, the Barclays US High Yield Index, a traditional cap-weighted index, is expected to return 2.2% over the next 10 years, after inflation and credit losses. The wide range of outcomes around the 2.2% central tendency falls between −0.3% and 4.7%.

Empirically robust and theoretically sound reasons support the belief that investors can do better than traditional high-yield index strategies. In fact, rules-based alternative strategies may go a long way toward capturing potential excess returns in the high-yield space. Such strategies follow two key principles, which mirror factor investing in equities, especially the intersection of quality and value, as discussed by Kalesnik and Kose (2014):

- Avoid the unrewarded risks of reaching for yield farther out on the credit-quality scale, and

- Take advantage of temporary mispricings by trimming recent winners and adding to recent losers.

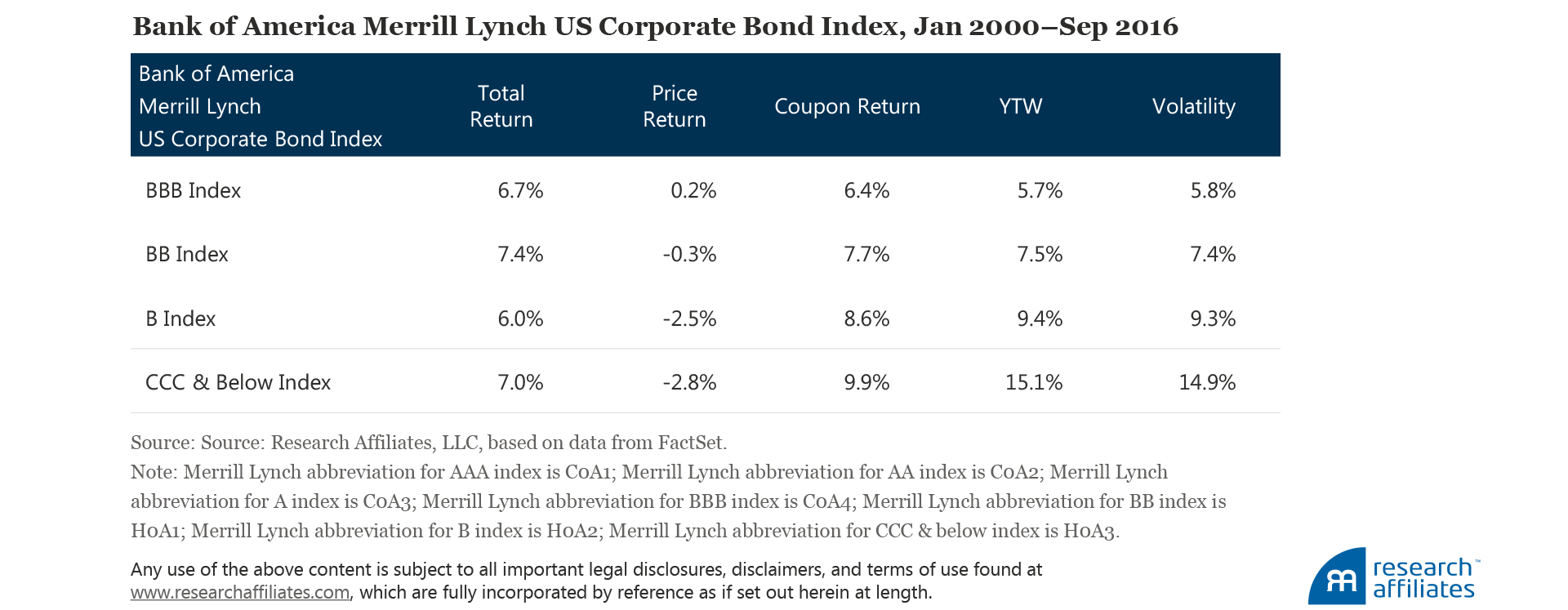

Avoid risks of reaching for yield. Looking at subsectors of the Bank of America Merrill Lynch US Corporate Bond Index in the almost 16 years ending September 30, 2016, we find that total returns do not follow a monotonic pattern of higher returns for worse-rated companies (B and below) versus better-rated high-yield credit (BBB and BB), whereas volatility grew by a factor of two to three times. In this instance, once credit losses from low-quality issuers are taken into account, more risk does not translate into better long-term return.

Take advantage of temporary mispricings. Price fluctuations across high-yield securities mean that a strategy of favoring recent losers relative to recent winners can add value over time, net of transaction costs. This approach is key to the discipline of systematic value investing. Investing in high yield is a complex endeavor, and implementing a high-yield index-based strategy requires both a substantial trading platform and a willingness to take on some tracking error relative to the benchmark. As is the case with substantially all bond index replication, the index represents more of a guide than an exact prescription for portfolio management.

Adopting the discipline of rebalancing bond exposures toward fundamental weights, which are linked to the economic size of the underlying issuing companies rather than to the amount of debt they have issued, achieves the dual objective of: 1) tilting holdings toward companies with better debt servicing and higher credit ratings; and 2) taking advantage of mean reversion in securities prices over time. A good example of the more conservative fundamental-weighting approach compares the $2.00 of BB-rated bonds for every $1.00 of B-rated bonds held in the RAFI Bonds US High Yield 1–10 Index to the $1.30-to-$1.00 ratio held in the Merrill Lynch US High Yield BB-B 1–10 Index.

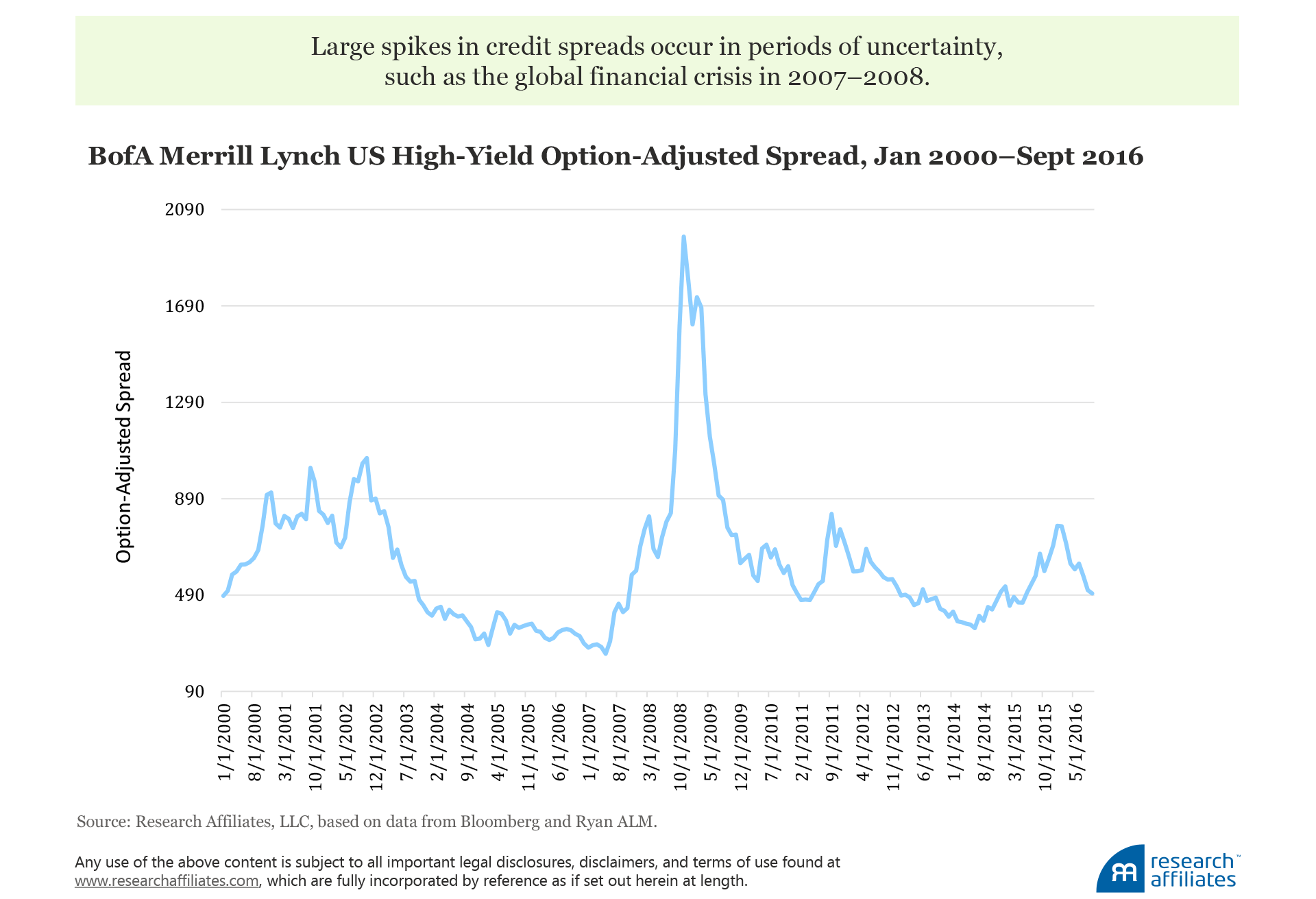

The unsurprising result would be that the RAFI index should outperform the Merrill Lynch index when credit spreads widen, and underperform when spreads narrow. Seemingly, this behavior might be construed as not leading to outperformance over time, because every spike in option-adjusted spread (OAS), a standard measure of the yield premium required by high-yield bondholders, would tend to eventually retract, and gains could easily be wiped out by symmetrical losses on the other side. This expectation turns out to be false.

In actuality, the periods of underperformance of the more conservative strategy generally do not undermine its overall ability to outperform. Two reasons account for this. First is the capture of a rebalancing premium by the fundamentally weighted strategy. As credit conditions change, corporate issuers experience different price responses, some more extreme than others, allowing for rebalancing into the temporarily cheap bonds of ultimately sound companies. The accumulation over time of realized pricing inefficiencies locks in long-term capital gains.

Second, the less conservative strategy in terms of quality must contend with large spikes in credit spreads that coincide with permanent capital losses on the shakiest of credits. The bonds of these companies contribute to underperformance as spreads widen, but the losses are never recovered for those companies that ultimately become insolvent.

The differences in the two strategies explain their differences in performance. A review of the period that began with the global financial crisis and the several years that followed shows the RAFI high-yield index produced approximately 7.8% in value-add relative to the Merrill Lynch index between June 2007 and November 2008 (the peak of the OAS spike), and only gave back 6.6% in the form of underperformance through April 2011, when OAS spreads next bottomed.

The recent shakeout and numerous defaults in the US shale energy industry offer another vivid example of the performance differences between the fundamental-weighting and cap-weighting approaches in high yield. Many small to midsized energy companies, such as Midstates Petroleum, SandRidge Energy, Goodrich Petroleum, and Patriot Coal, were highly levered, having fueled their growth with piles of fresh junk debt in the early 2010s.

With crude oil and petroleum derivatives still down significantly from the highs of mid-2014, and a year-plus into the painful process of debt restructurings, defaults, and bankruptcies, the RAFI Bonds US High Yield 1–10 Index delivered 90 basis points (bps) of excess return in 2015 and 50 bps in 2016, through September, relative to the Merrill Lynch US High Yield BB-B 1–10 Index. The RAFI index has outperformed without being systematically underweight the energy sector as a whole, just that segment of the market which had bigger growth aspirations than its current economic size could shoulder.

Conclusion

Long-term bond investors may be uncomfortably stuck between the high returns of the past and the much lower and potentially negative returns of the future, but we can position our portfolios to produce excess returns versus their respective benchmarks, both government and credit. The present offers long-term fixed-income investors a likely higher degree of comfort if we select a strategy that maintains investment discipline and seeks pricing inefficiencies, while even adopting a relatively more conservative quality stance than a traditional cap-weighted index.

Endnotes

- Marks 2016 offers additional reading on how economic reality plays a role, eventually, in the functioning of the economy and financial markets.

- The asset-buying program of the Bank of Japan (BOJ) has been so substantial it has left interest rates squarely in negative territory and has created a problematic shortage of JGBs in the marketplace, as the BOJ actively competes with large institutions for existing bonds (Kawa, 2016).

- Being underweight a country such as Japan in a smart beta index can be uncomfortable, but is not comparable to being outright short JGBs in the decades-old widow-maker trade favored at times by various hedge funds. Arnold (2015) describes the widow maker and its potential for investment performance death and destruction. Indeed, although the short-term pain of being underweight Japanese sovereigns may be quite real, the potential for long-term reward is strong for investors with long-term horizons.

References

Arnold, Wayne. 2015. “Don’t Be Tempted by Japan’s Widow Maker.” Barron’s (November 20).

Brightman, Chris. 2016. “Death of the Risk-Free Rate.” Research Affiliates, July.

Kalesnik, Vitali, and Engin Kose. 2014. “The Moneyball of Quality Investing.” Research Affiliates, June.

Kawa, Luke. 2016. “Japan Is Fast Approaching the Quantitative Limits of Quantitative Easing.” Bloomberg (April 6).

Marks, Howard. 2016. “Memo to Oaktree Clients: Economic Reality.” Oaktree Capital Management, LP (Addendum dated June 13).

Shepherd , Shane. 2014. “The Outlook for Emerging Market Bonds.” Research Affiliates, July.