Systematic rebalancing raises the likelihood of improving long-term risk-adjusted investment returns.

The benefits of rebalancing result from opportunistically capitalizing on human behavioral tendencies and long-horizon mean reversion in asset class prices.

Investors who “institutionalize contrarian investment behavior” by relying on a systematic rebalancing approach increase their odds of reaping the reward of rebalancing.

Introduction

Embracing a disciplined approach to rebalancing can lead to better long-term investment outcomes. Overcoming the natural tendency to wait-and-see before repositioning our portfolios can be a difficult, but worthy, goal for investors to pursue. Advisors can help investors surmount this and other behavioral hurdles by adopting a systematic rebalancing approach that effectively institutionalizes contrarian investment behavior.

This is the eighth and last article in a series that focuses on the investment role of financial advisors. Previously, we have discussed the major contributors to successfully meeting the long-term financial goals of investors: starting yield, risk, diversification, manager selection, portfolio construction, performance measurement, and taxes.

According to a recent Wells Fargo/Gallup Survey,1 31% of investors would opt to spend an hour stuck in traffic rather than spend that time rebalancing their portfolios. Why would we subject ourselves to gridlock instead of performing a simple task such as rebalancing a portfolio? With our office near Los Angeles, the most congested city in the world,2 we are certainly no strangers to traffic, so we will venture a guess.

It may well be that for many investors, rebalancing feels worse than rush hour. When we're stuck in traffic, at the very least we’re in the comfort of our cars and can find other productive ways to pass the time, such as listening to the radio, podcasts, or audiobooks. In contrast, rebalancing forces us to endure the discomfort of buying assets that have just inflicted pain from underperformance and of selling recent winning assets.3 Even worse, rebalancing our portfolios may induce additional pain if momentum carries prices further from fair value. On the highway, our GPS provides helpful estimates of our arrival time, but no GPS is available to pinpoint when market cycles will end: fair value may take months, years, and sometimes even decades to assert itself.

But if we broaden our perspective beyond the salience of the here-and-now to focus on what will ensure our long-term physical and financial well-being, the picture flips. Over time, traffic congestion inadvertently leads to damaging effects on our wallets, health, and environment.4 In contrast, a disciplined rebalancing approach continually positions our portfolios to reduce risk, raising the likelihood of our being able to improve risk-adjusted returns over those of an asset mix whose weights drift with price movements. In short, consistent rebalancing is a reliable, and often underappreciated, source of higher risk-adjusted performance for the patient investor.

The Rewards of Disciplined Rebalancing

Because rebalancing our portfolios may induce pain, and even punish us with short-term losses, it becomes even more crucial to keep the end destination—to increase the likelihood of our achieving better investment outcomes over time—forefront in our minds.

Rebalancing allows an investor to maintain the desired risk exposure of a portfolio over its life. The expected volatility of a portfolio with an initial 60/40 allocation to stocks and bonds will change if a bull market in equities has pushed its asset mix to 80/20. According to the Research Affiliates Asset Allocation Interactive (AAI) tool on our website, as of June 30, 2018, a 60/40 portfolio has an expected volatility of 8.6% compared to 11.4% for an 80/20 portfolio—a 30% increase in volatility! By regularly rebalancing portfolios, investors can maintain an exposure to risk that matches their tolerance.

Along with reliably reducing risk, rebalancing also has the potential to increase return. Over the long run, a rebalanced mix delivers better risk-adjusted returns compared to an asset allocation that merely drifts with price movements. As we will discuss later in the article, the benefits of rebalancing arise from opportunistically capitalizing on human behavioral tendencies and from long-horizon mean reversion in asset class prices.5

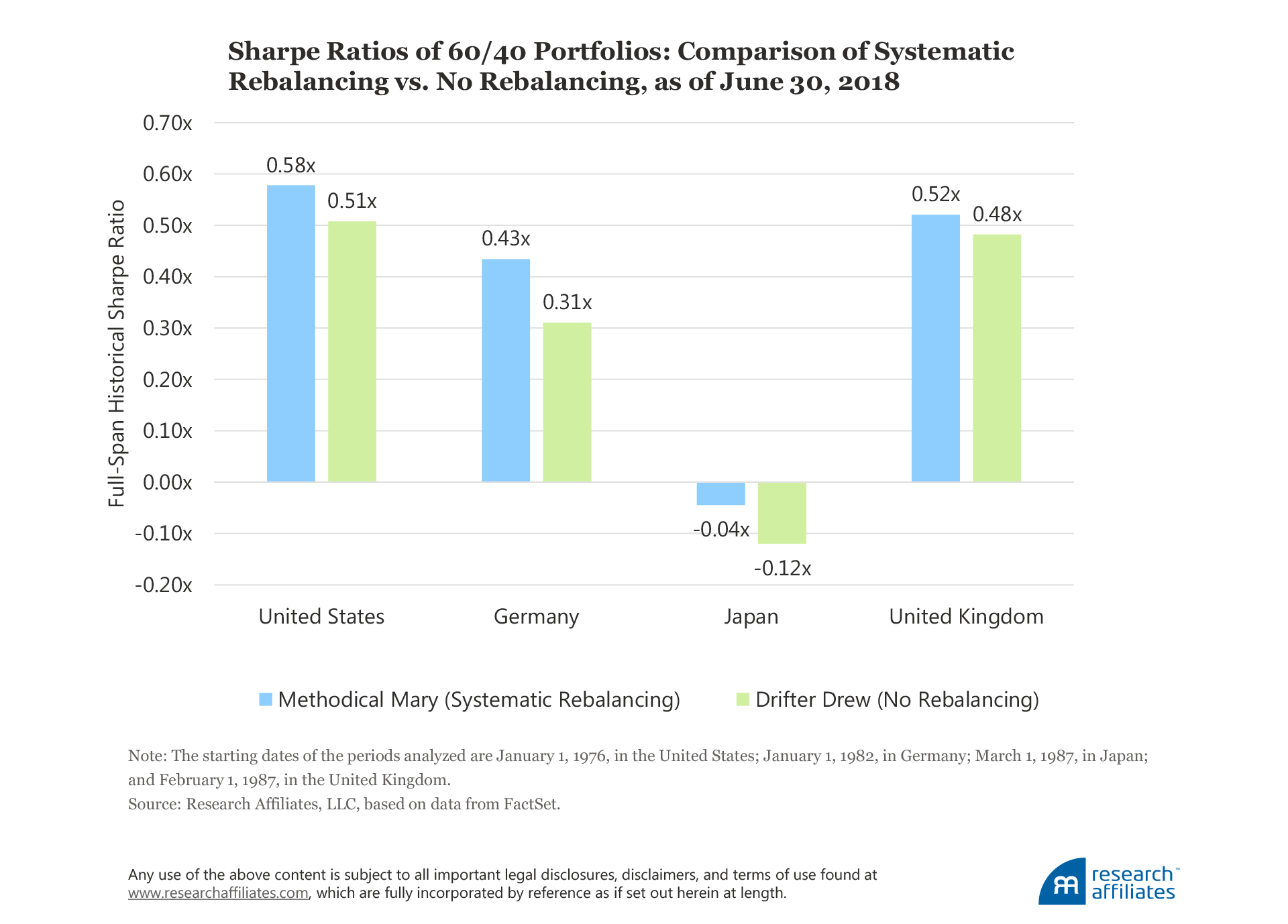

A quick study of two investor portfolios illustrates how a simple rebalancing practice can improve a portfolio’s risk-adjusted performance over time. For simplicity we assume each portfolio begins with the classic 60/40 mix of core stocks and bonds, although we acknowledge the benefit from rebalancing may rise as market breadth increases (Aked et al., 2017) or when rebalancing is applied within an asset class. We show the results across four major developed countries for time spans through June 30, 2018: United States, Germany, Japan, and United Kingdom.6

The disciplined investor who systematically rebalances on an annual basis7 is Methodical Mary. Without fail, Mary brings her asset mix back to the initial 60/40 allocation at the end of each year. At the other end of the spectrum is Drifter Drew, who also begins with a 60/40 stock/bond allocation, but who lets his portfolio price drift8 without ever rebalancing.

We observe a benefit from systematic rebalancing in each of the four geographies over the respective time spans we analyzed. Methodical Mary’s adherence to her predetermined plan beats Drifter Drew’s hands-off approach in each case.

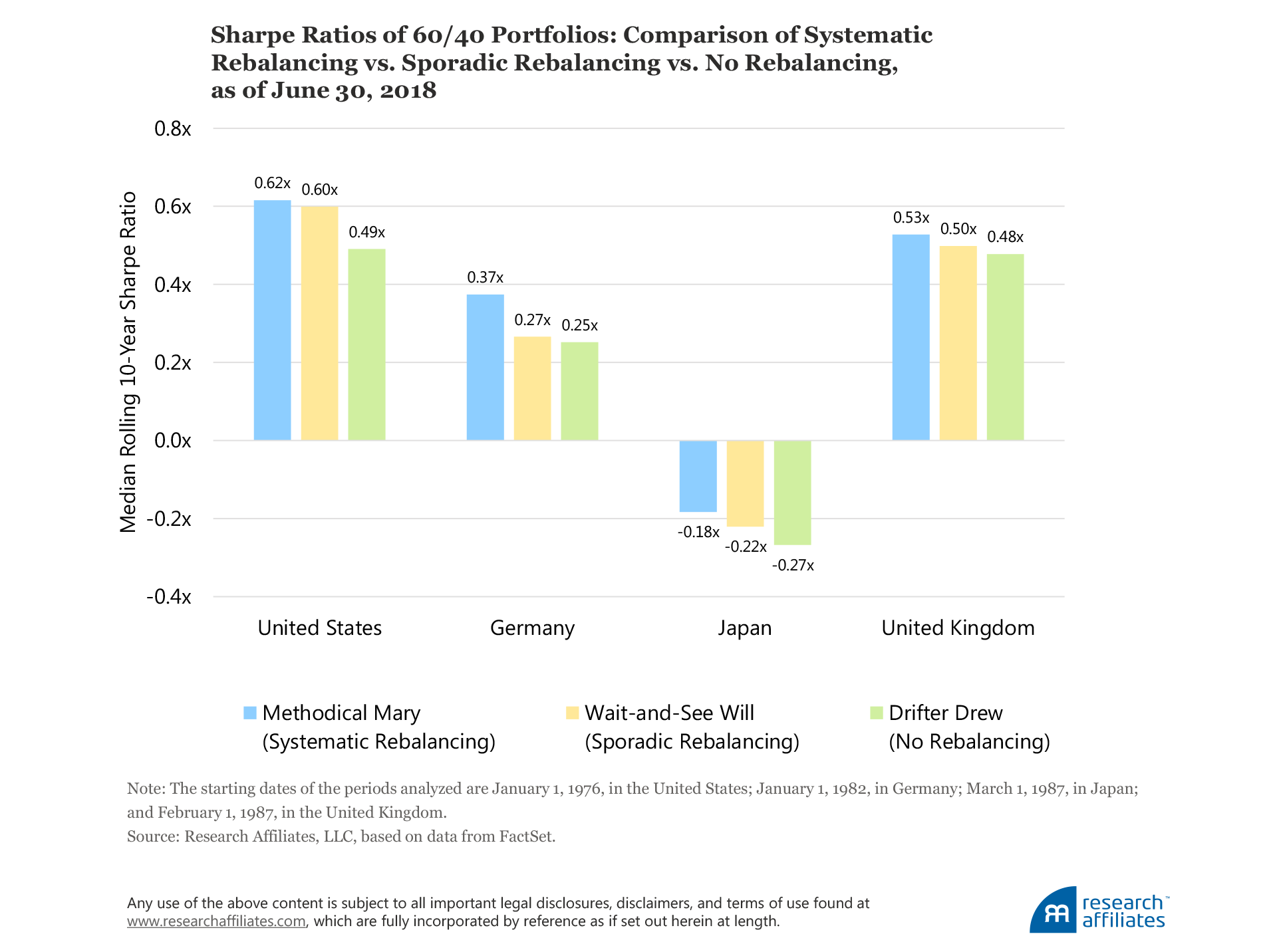

Is a Wait-and-See Approach Better?

The Drifter Drew example is a little extreme. Rarely does an investor allow their portfolio’s asset mix to drift with market prices for decades on end with no adjustment whatsoever. The final price-drifted portfolio’s mix would be quite dissimilar from its original asset allocation. A far more realistic scenario is one epitomized by an investor we call Wait-and-See Will, who in times of volatile market movements waits for clarity on the market’s direction before deciding to rebalance. Buying into a cratering market feels precarious and dangerous to Will, so he waits a bit before rebalancing. Similarly, when equities are on a tear, he holds off before trimming his appreciating exposure. At face value, this approach is not only familiar, but seems sensible, credible, and prudent.

Our behavioral tendencies play a role in our decisions related to rebalancing because we are evolutionarily wired to follow the herd. No one wants to be wrong and alone. In fact, if we are not one ourselves, many of us know a Wait-and-See Will, who seeks safety in numbers rather than be comfortable in marching to a different drummer. We all have a fear of missing out (popularly known as FOMO) by not making the same “right” decision that our neighbor makes. As the economic historian Charles Kindleberger stated, “There is nothing so disturbing to one’s well-being and judgment as to see a friend get rich” (presumably when you are not likewise so lucky).

Another reason the Wait-and-See Will approach is prevalent among investors is because so many of us are susceptible to the house-money effect when making decisions about our portfolios. Kahneman and Tversky (1973) introduced the representativeness heuristic, which describes how “similarity” or “representativeness” is mistakenly used as a substitute for statistical thinking. Its application leads to many mistakes in judgment, including the tendency to extrapolate from recent evidence and to exhibit confirmation bias. Even if we could magically suppress human behavioral foibles, the most rational of us would still find it hard to rebalance.9 Chalk it up to the house-money effect: when our portfolio value rises in up markets, we can become too risk seeking and fail to trim our allocations of rallying assets.

So, let’s compare Will’s approach to those of Methodical Mary and Drifter Drew over a reasonable longer-term investment horizon of rolling 10-year periods.10Although the wait-and-see approach can take a number of forms, for simplicity we assume that when stocks rise or fall by more than 20% over a 12-month period, Will skips the next annual rebalance. We do not impose a limit on the number of rebalances he can skip. Will waits to rebalance until the +/− 20% return threshold is no longer triggered, which to many investors would reflect a return to some semblance of market normalcy.

As an example, let’s rewind the clock to the global financial crisis. In the 12-month period ending September 30, 2008, US stocks fell by 22%. Amid this strong decline, Will decides not to rebalance his portfolio back to its 60/40 target allocation on the next annual rebalance date of December 31, 2008. Therefore Will's portfolio mix ends the year with 45% in equities and 55% in bonds. The following year stocks begin a swift and strong recovery. In the 12-month period ending November 30, 2009, US stocks rebound by over 25%, once again crossing the 20% threshold. Will again opts to forgo rebalancing at the end of 2009, leaving his portfolio mix at 50/50 rather than 60/40. Following this pattern, for the time periods analyzed through June 30, 2018, Wait-and-See Will’s portfolio is prey to price drift, skipping annual rebalancing from a low of 74% of the time (in the United States) to a high of 90% of the time (in Japan).

Based on this approach, although Wait-and-See Will generally gains more than Drifter Drew on a risk-adjusted return basis, Methodical Mary still emerges as the winner. The improvement in each portfolio’s risk–return profile is reflected by an increase in the average rolling 10-year Sharpe ratio, which ranges from a 10% rise in the United Kingdom (0.48x to 0.53x) to a 48% rise in Germany (0.25x to 0.37x). These results suggest that investors who systematically rebalance may be rewarded with better risk-adjusted returns than their peers who rebalance either sporadically or not at all.

Not only does Methodical Mary’s portfolio exhibit superior 10-year risk-adjusted returns over the entire analysis period, the systematic rebalancing in her portfolio leads to improved outcomes delivered reliably. We acknowledge that the 10-year rolling periods we use in our analysis include non-independent, overlapping periods, and with the earliest start date in 1976, the number of independent 10-year spans is, at most, four. Noting this caveat, however, Mary’s systematic rebalancing beats Will’s sporadic rebalancing and Drew’s lack of rebalancing in more than 79% of the rolling 10-year periods over all four markets we study. The odds of risk-adjusted outperformance are overwhelmingly in Methodical Mary’s favor.

Conclusion

Technology may have the potential to alleviate traffic. Autonomous cars may be able to efficiently manage traffic flow. Elon Musk’s Test Tunnel may allow some commuters to bypass traffic on surface streets altogether. While exciting and newsworthy, these solutions have not been completely tested and proven. Conversely, while systematically rebalancing our portfolios is mundane, it has been proven effective.

So how can advisors help their clients understand this finding and adopt it as part of their investing approach? A necessary first step is recognizing the natural behavioral tendencies to which we too easily succumb—but awareness alone is insufficient to produce the best results. Taking a proactive approach, such as applying rules-based rebalancing devoid of emotion and subjectivity can vastly improve investing outcomes. Like Methodical Mary, advisors and their clients may be best served by formalizing a rebalancing framework and “institutionalizing contrarian investment behavior”11 to maximize the odds of reaping the proven benefits of portfolio rebalancing.

Endnotes

- These findings are part of the Wells Fargo/Gallup Investor and Retirement Optimism Index conducted July 28–August 6, 2017, by telephone.

- According to an analysis published annually by Inrix of 1,360 cities, Los Angeles is the most congested city in the world, followed by New York City and Moscow (Korosec, 2018).

- As Lovell and Arnott (1989) discussed, multiple factors suggest when portfolio rebalancing is timely and appropriate: changes in market prices and return prospects; changes in client objectives; new investment alternatives; and macroeconomic changes. Although all are important considerations, in this article we focus on the first.

- These costs include the tangible and direct cost of fuel, which totaled nearly $305 billion for US drivers in 2017. And although we may have the illusion of being productive or relaxing while sitting in traffic, we are nevertheless deprived of the option of more practical or more desirable ways to spend our time. Finally, traffic congestion negatively impacts the levels of air pollution and creates other health risks; the reality is that we are compromising our health and leaving our environment worse off for future generations (Zhang and Batterman, 2013).

- As Malkiel (2015) put it, “We all wish some genie could tell us when the stock market tops out so we could sell. Rebalancing is the closest technique available to do that.”

- The representative indices we use in our analysis are, for the US markets, S&P 500 Index and Barclays US Aggregate; for Germany, MSCI Germany Index and Barclays Global Germany (5–7Y); for Japan, MSCI Japan Index and Barclays Global Japan (5–7Y); and for the United Kingdom, MSCI United Kingdom and Barclays Global UK (5–7Y).

- Our research findings indicate the highest extra-return benefit by rebalancing occurs over the holding period of highest volatility, which occurs at one year (Aked and Ko, 2017). In addition, research suggests that annual rebalancing is preferable compared to more-frequent rebalancing, after accounting for taxes, transaction costs, and labor costs (Jaconetti, Kinniry, and Zilbering, 2010).

- In our simple analysis, we do not account for the costs associated with a rebalancing strategy, such as taxes and transaction costs, which may slightly reduce the end return investors receive. Beyond the scope of this paper, there are strategies to minimize the associated costs, such as rebalancing a portfolio with cash flows to trim rebalancing costs.

- Hsu (2012) provides more information on, and an example of, how changing risk aversion influences investors’ lack of interest in rebalancing.

- Ten years is a fairly representative horizon for investors and is also the time horizon used in the All Asset Interactive (AAI) tool.

- The expression to “institutionalize contrarian investment behavior” comes from Ang and Kjaer (2011), who argued this is the best approach for investing counter-cyclically. Rebalancing, at its core, is investing counter-cyclically. Interested readers can find examples and suggestions to improving rebalancing rules in Section 3.1 of Ang and Kjaer.

References

Aked, Mike, Rob Arnott, Omid Shakernia, and Jonathan Treussard. 2017. “Hobbled by Benchmarks.” Journal of Portfolio Management, Multi-Asset Special Issue, vol. 44, no. 2 (December):74–88.

Aked, Michael, and Amie Ko. 2017. “Time Diversification Redux.” Research Affiliates Publications (August).

Ang, Andrew, and Knut Kjaer. 2011. “Investing for the Long Run.” In A Decade of Challenges: A Collection of Essays on Pensions and Investments, edited by Tomas Franzen. Stockholm: Andra AP-fonden, Second Swedish National Pension Fund: 94-111.

Hsu, Jason. 2012. “Why We Don’t Rebalance.” Research Affiliates Fundamentals(July).

Jaconetti, Colleen M., Francis M. Kinniry, Jr., and Yan Zilbering. 2010. “Best Practices for Portfolio Rebalancing.” Vanguard Research (July).

Kahneman, Daniel and Tversky, Amos. 1973. “Availability: A Heuristic for Judging Frequency and Probability.” Cognitive Psychology, vol. 5, no. 2 (September):207–232.

Korosec, Kirsten. 2018. “The 10 Most Congested Cities in the World.” Fortune(February 6).

Lovell, Robert, and Robert Arnott. 1989. “Monitoring and Rebalancing the Portfolio.” Investment Management Reflections No. 3, First Quadrant Corporation.

Malkiel, Burton. 2015. “A 2015 ‘Rebalancing’ Act for Investors.” The Wall Street Journal (December 30).

Zhang, Kai, and Stuart Batterman. 2013. “Air Pollution and Health Risks Due to Vehicle Traffic.” Science of the Total Environment, vols. 450–451 (April 15): 307–316.